Mortgage and Loan Product Maintenance

Product maintenance menu allows you to maintain the details of Mortgage and Loan Products that are offered by your bank to its customers. Once the Product is created, the values in these Products are defaulted to the loan accounts that are created under the Product, with an option to change the details at the account level.

The following are the tabs in a Mortgage and Loan Product and are aggregated under these tab heads:

PROFILE

PRICING

REPAYMENT

ACCOUNTING

CUSTOM FIELD

Creating a Mortgage and Loan Product

To create a new Mortgage and Loan Product,

1. Access Retail menu, click Settings, and then Product. The Product Search page appears. All Products available in Aura appear on the page.

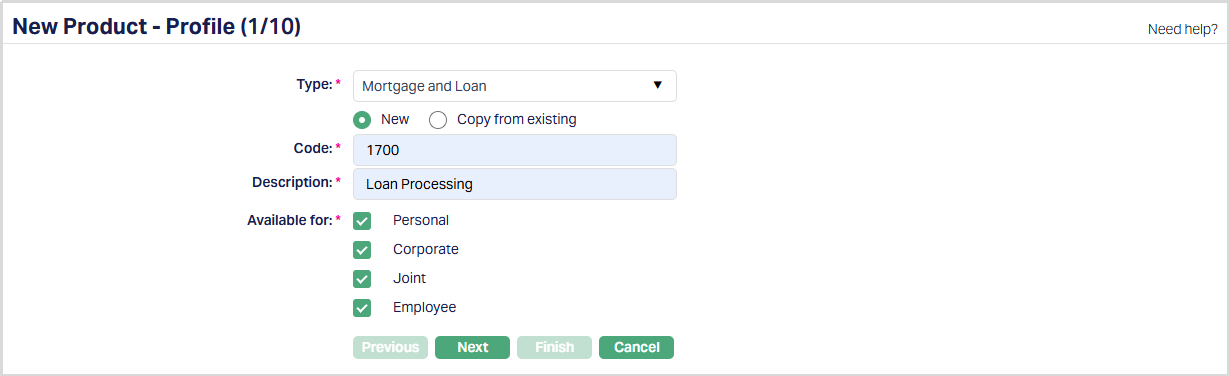

2. Click Add. The New Product → Profile (1/10) appears.

3. Select Mortgage and Loan as the Type from the drop-down list for the Product.

4. Aura allows you to create a new loan Product from scratch or create a loan Product based on already existing loan Products.

To create a new Product, select New.

If you want to create a loan Product based on the properties of an existing loan Product, then select Copy from existing.

5. On selection of Copy From Existing, Copy from drop-down list is displayed with the list of all Mortgage and Loan Products already existing. Select the required Product to copy from. All the values in the next steps are defaulted from that Product; and you can make the required changes.

Note: Certain fields where the value should be unique are left blank so that you can input the required values. Example: Code

6. Enter the Code for the Product. The Product Code has to be unique across all Products for the Entity.

7. Enter the Description for the Product.

8. Select the option for Available for field. This will determine the type of clients to which the Product will be available. The options are:

- Personal → Single person

- Corporate → Organisations or companies

- Joint → Group of two or more persons

- Employee → Employee of the bank.

Note: For Mortgage loans, the Personal option is checked by default. You can uncheck the same and / or check the required checkboxes for Corporate or Employee and / or Joint ownership.

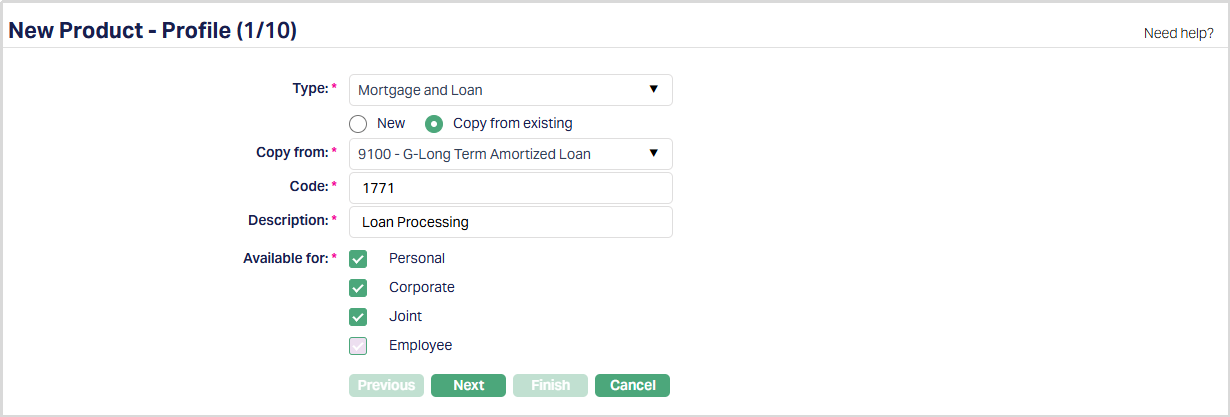

9. Click Next. The New Product → Currency (2/10) page appears.

10. Select the Currency for the Product from the drop-down list of GL currencies that have been defined as Not a Commodity under Admin →> Currency definition. More currencies can be added during Edit using the Currency tab, once the Product record is created. Loan accounts for the Product can be opened only in such currencies that are mapped to that Product.

11. Enter the Minimum loan amount for the loan accounts under the Product for the above currency.

12. Enter the Maximum loan amount for the loan accounts under the Product for the above currency. The Maximum Loan Amount should be greater than the Minimum Loan Amount.

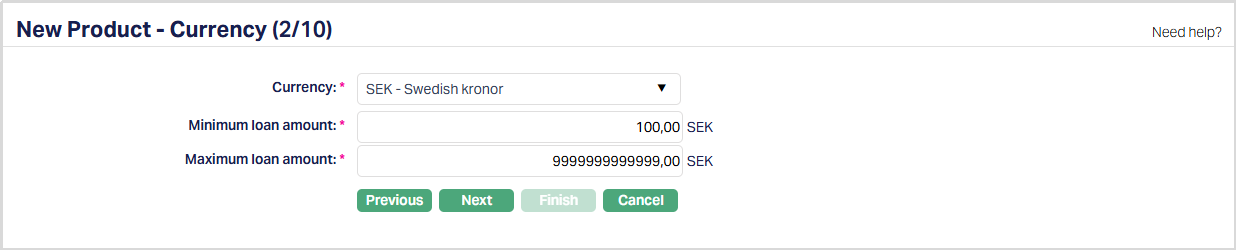

13. Click Next. The New Product → Settings (3/10) page appears.

14.Click Yes or No radio button for IBAN generation required for this Product. During account creation under the Product, if this has been selected as Yes, Aura will automatically create IBAN according to the IBAN format maintained at the Entity level.

15. Enter the minimum number of days for loans under this Product in Minimum term days. This should be a positive integer between 1 and 99999

16. Enter the maximum number of days for loans under this Product in Maximum term days. This should be a positive integer between 1 and 99999 and also should be greater than or equal to Minimum Term Days

17. Enter the number of days after which the penalty interest or late payment fees for any payment defaults will start applying in Grace days for penalty. By default, this is set to 0; and in such a case, the penalty interest or late payment fee will be applied on the Payment Due Date in case of any payment default.

18. Select the type of days for the Grace days for penalty. The preshipped options available in the dropdown list are:

Calendar days → If this is selected, then all the calendar days will be counted for Grace Days For Penalty, including the holidays.

Business days → If this is selected, then only working days, i.e., days excluding the holidays as defined in the Account Branch of the Loan will be counted for Grace Days For Penalty.

Note: If Grace Days for Penalty is defined as Business Days, then the field Holiday Preference(Grace Days for Penalty) will not be applicable as the Grace Days will never end on a Holiday; and hence, will be disabled.

19. Select Interest calculation method from the pre-shipped drop-down. Available options are:

Amortized Under this, the Loan Principal is spread out into a series of fixed payment amounts that you can specify. You have the ability to set different frequencies for Interest and Principal payment. The interest calculation will be based on the outstanding principal at the beginning of the period and is calculated based on the amount and length of time period.

Annuity Annuity is a payment option where the repayment interval and the amount of repayment are fixed. Aura will automatically split the required repayment amount between Principal and Interest and you cannot change the same.

20. If Annuity is selected as your Interest Calculation Method, then On prepayment field will be available. You can choose to Revise Annuity or Revise Tenor. If you select Revise Annuity, and if there are any changes to the terms of the loan contract, the Tenor of the loan remains the same and the Annuity is appropriately recalculated. On the other hand, if Revise Tenor is selected, then, during change of terms, the Annuity of the loan contract remains the same and the tenor of the loan is suitably adjusted.

21. Select Rate type for disbursement from the drop-down list of rate types maintained under Admin → System codes → Currencies → Currency rate type. This is the rate type to be used when the Loan Account Currency and Disbursement Currency are different

22. Select Rate type for repayment from the drop-down list of rate types maintained under Admin → System codes → Currencies → Currency rate type. This is the rate type to be used when the Loan Account Currency and Repayment Account Currency are different.

23. Select Rate type for charge from the drop-down list of rate types maintained under Admin → System codes → Currencies → Currency rate type. This is the rate type to be used when the Loan Account Currency and Charge Account Currency are different and also if the Charge Currency created at charge level is different.

24. Indicate if the loans under this Product should be Secured or not using the radio buttons. If this has been selected as Yes, the next field Minimum Secured Percentage will be enabled.

25. Enter the Minimum secured percentage for the Product. Minimum Secured Percentage denotes the percentage applied on the exposure amount (i.e., the Loan amount) up to which the loan has to be secured by collateral / limit for the Loan Account Activation to be successful.

Example:

Loan Amount = EUR 100 000.00

Minimum Secured Percentage = 75%

Loan Account can be activated only when the mapped collateral / limit amount >= EUR 75 000.00

27. Enter the Minimum interest rate for the loan accounts under the Product.

28. Enter the Maximum interest rate for the loan accounts under the Product. Maximum Interest Rate should be greater than the Minimum Interest Rate.

Note: If the Final Interest Rate in the Loan Account falls beyond the Minimum / Maximum interest rate specified here, Aura will automatically use these Minimum / Maximum interest rates appropriately to calculate the Loan's interest

29.Enter the Minimum annuity schedule amount. This field is displayed only if the Interest Calculation Method is selected as Annuity. When the threshold is mentioned, during Payment Schedule generation, if the total outstanding amount in the last schedule is less than the threshold for Minimum annuity schedule amount, then Aura adds the minimum annuity schedule amount in previous schedule.

30. Enter the threshold amount for closure of a loan account in Threshold for closure field. At EOD, if the total receivable amount is less than threshold amount for closure, then Aura will pass threshold entries for the account and will close loan account.

31. Threshold for Own Account Auto Repayment is used to define the minimum amount that should be available in the borrower's Client Account that has been linked to the Loan Account to trigger the automatic repayments. If the available balance in the linked Client Account is less than the amount specified here, automatic repayment will not be initiated.

32. Select the holiday preference for payments from the Holiday preference (Payment) dropdown list. This will determine the Payment Due On date (the actual date on which the payment will be initiated from the linked Client Account). The options available are:

Ignore

When this preference is selected, No holiday preference will be applicable for loan accounts under this Product. All Payment Due Dates will remain the same, irrespective of whether it is a working day or a holiday.

During Schedule generation, if the payment day is a holiday then the Payment Due On date will remain the same and payment is to be initiated / accepted on the same day.

Next business day

- When this preference is applied to the loan account, On payment schedule generation, Aura will check if the payment day is a holiday. If yes then the Payment Due On date for the repayment is updated with next business date.

Previous business day

- Similar to Next business day; but, here, the Payment Due On date will be the previous business day when holiday is encountered.

Example:

Holidays: 25-Dec-2025, 26-Dec-2025, 27-Dec-2025, 28-Dec-2025

Schedule's Payment Due Date: 26-Dec-2025

Payment Due On Date will be as follows for the different Holiday Preferences:

| Preference | Payment Due On Date |

|---|---|

| Ignore | 26-Dec-2025 |

| Next business day | 29-Dec-2025 |

| Previous business day | 24-Dec-2025 |

32. Enter the holiday preference for grace days for penalty from the Holiday preference (Grace days for penalty) dropdown list. This field specifies the holiday treatment to be applied when the End of Grace Days happens to be a holiday. This field is disabled if Grace Days For Penalty is defined as Business Days. The late payment fee / penalty calculation will start based on this treatment, but with effect from the Due Date. The options available are:

Ignore

- If the day on which the grace days end is a holiday, then the same day is treated as end of grace day to calculate penalty.

Next business day

- If the end of grace days happens to be a holiday, then Aura will postpone till next business day and start calculating the penalty from that day, but, with effect from the Payment Due Date.

Previous business day

- Similar to Next business day except that the previous business day is considered when holiday is encountered.

Example:

Holidays: 25-Dec-2025, 26-Dec-2025, 27-Dec-2025, 28-Dec-2025

Schedule's Payment Due Date: 26-Dec-2025

Grace Days: 2 calendar days End of Grace Days will be as follows for the different Holiday Preferences:

| Preference | End of Grace Days |

|---|---|

| Ignore | 28-Dec-2025 |

| Next business day | 29-Dec-2025 |

| Previous business day | 24-Dec-2025 |

33. Select the holiday preference for periodic interest re-pricing from the Holiday preference (Periodic interest re-pricing) dropdown list. This determines the actual date for the interest re-pricing if the upcoming reset date falls on a holiday. The options available are:

Ignore

- When this preference is selected, then no holiday preference will be applicable for loan accounts under this Product for any Interest Re-pricing (LNRATE) to be done; and Interest will be reset on that day.

Next business day

- When this preference is applied Aura will check if the next Interest Re-pricing (LNRATE) reset date is a holiday. If yes, then the book date and value date for the event will be updated with next business date.

Previous day

- Similar to Next business day, except that the previous business day is considered when a holiday is encountered.

Example:

Holidays: 25-Dec-2025, 26-Dec-2025, 27-Dec-2025, 28-Dec-2025

Next Interest Reset Date: 26-Dec-2025

The Interest Reset Date will be as follows for the different Holiday Preferences:

| Preference | Interest Reset Date |

|---|---|

| Ignore | 26-Dec-2025 |

| Next business day | 29-Dec-2025 |

| Previous business day | 24-Dec-2025 |

34. Include Disbursement Charges in Loan Amount can be used to indicate if the Loan Amount should be enhanced by the initial disbursement related charges. When this is set to Yes, the Approved Amount of any loan account that is created under this Product would automatically be increased by the amount of charges that is applied at the time of the first disbursement. When this is set to No, there is no such increase in the loan's Sanctioned Amount.

Disbursement Charges: The following charges defined in the Loan Account → Default Charges Tab along with any Adhoc Charges applied on the account before the first disbursement will be considered as Disbursement Charges:

- Processing Fee

- Service Charge

- Documentation Charge

- Legal Charge

- Appraisal Charge

- Lender Inspection Charge

- Credit Report Charge

- Notary Charge

- Stamp Charge

36. Net receivables during disbursement enables you to define if the disbursement charges should be netted off during the first disbursement, or if they should be part of the first Payment Schedule / Invoice. If this is checked, then any disbursement charges applicable for an account will be collected during the disbursement and only the net disbursement amount will be credited to the borrower. The checkbox can be unchecked to indicate that the disbursement charges will not be deducted during disbursement; but will be included in the upcoming schedule / invoice.

If the above field (Include Disbursement Charges in Loan Amount) is set to No, by default the Net receivables during disbursement checkbox is unchecked; and you can check it if required.

If the above field (Include Disbursement Charges in Loan Amount) is set to Yes, by default the Net receivables during disbursement checkbox is checked and disabled. This is to ensure that the disbursement charges are netted off during disbursement when the loan's Approved Amount is increased to include such charges.

38. Include Disbursement Charges in Annuity is enabled only if Interest Calculation Method = Annuity; and only if Include Disbursement Charges in Loan Amount = No. By default, this field is set to No and can be changed to Yes. If this field is set to Yes, the Annuity Amount will be calculated based on the Approved Amount plus the Disbursement Charges; and the schedules will be generated to ensure that the Principal repayment starts only after the Disbursement Charges are paid. Interest for such period till the Principal repayment starts will however continue to be included in the schedule as usual.

If this field is set to No, the Annuity amount will be calculated based on the Approved Amount only; and the schedules will be generated using the Annuity Amount split between Interest and Principal; the Disbursement charges will be either netted off during disbursement or included in the upcoming schedule, based on the Net Receivables During Disbursement.

If Interest Calculation Method = Annuity and Include Disbursement Charges in Loan Amount = Yes: This field is set to No and disabled.

40. By default, the Generate Schedules for Full Tenor checkbox is unchecked, and the schedules will be generated for only 12 schedules. When this checkbox is checked, the schedules will be generated for the entire loan tenor.

41. Click Next. The New Product → Interest Receivable (4/10) page appears.

39. Select the Loan Interest scheme that would be applicable to the accounts under this Product from the drop-down list of Interest schemes maintained under Admin → Pricing → Interest → Interest Scheme. The interest receivable on the principal amount would be derived using this scheme.

40. Select the Principal overdue scheme from the drop-down list of Interest schemes maintained under Admin → Pricing → Interest → Interest Scheme. The penalty receivable on the principal overdue (i.e., the principal amount which was due but has not been received from the client even after the grace days) would be calculated using this scheme.

41. Select the Interest overdue scheme from the drop down. Interest schemes should have been maintained under Admin → Pricing → Interest → Interest Scheme. The penalty receivable on the Interest overdue (i.e., the Interest amount which was due but has not been received from the client even after the grace days) would be calculated using this scheme.

42. Click Next. The New Product → Charges (5/10) page appears.

43. If you want to levy a charge for processing the loans under this Product, select the Processing fee from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

44. When you want to levy Service charges for the loans under this Product, select the Service charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

45. When you want to levy a Documentation charge, select the Documentation charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

46. When you want to levy a Legal charge, select the Legal charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

47. When you want to levy a Prepayment charge on Principal repayments made before their due dates, select the Prepayment charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No, Treat as Receivable = No and Amortization is set as No. If the Charge is Banded, the charge amount will be calculated on the basis of the Principal amount prepaid. This charge will be collected when user does a prepayment using the Loan Repayment Screen.

48. When you want to levy an Installment fee, select the Installment fee from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No, Treat as Receivable = No and Amortization is set as No. If the Charge is Banded, the charge amount will be calculated on the basis of the amounts due for Principal and Interest. The charge amount is collected for every installment and will be shown as a separate charge schedule for every Due Date when Principal and / or Interest is due.

49. When you want to levy a Late payment fee, select the Late payment fee from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No, Treat as Receivable = No and Amortization is set as No. If the Charge is Banded, the charge amount will be calculated on the basis of the overdue amount of Principal and Interest. The charge is applied on the End of Grace Days and is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

50. When you want to levy an Additional disbursement charge, select the Additional disbursement charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the Principal amount that is being disbursed. The charge amount is collected when ever an additional disbursement is done, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

51. When you want to levy Appraisal charges for the loans under this Product, select the Appraisal charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

52. When you want to levy Lender inspection fee for the loans under this Product, select the Lender inspection charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

53. When you want to levy fee for sending reports for the loans under this Product, select the Credit report charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

54. When you want to levy charges on identity verification by Notary for the loans under this Product, select the Notary charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

55. When you want to levy charges on registration for the loans under this Product, select the Stamp charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected upon disbursement, if Net Receivables during disbursement = Yes; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

56. When you want to levy fee for managing the loans under this Product, select the Loan Management charge from the drop-down list of all the Active Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No and Treat as Receivable = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. The charge amount is collected for every installment and will be shown as a separate charge schedule for every Due Date when Principal and / or Interest are due.

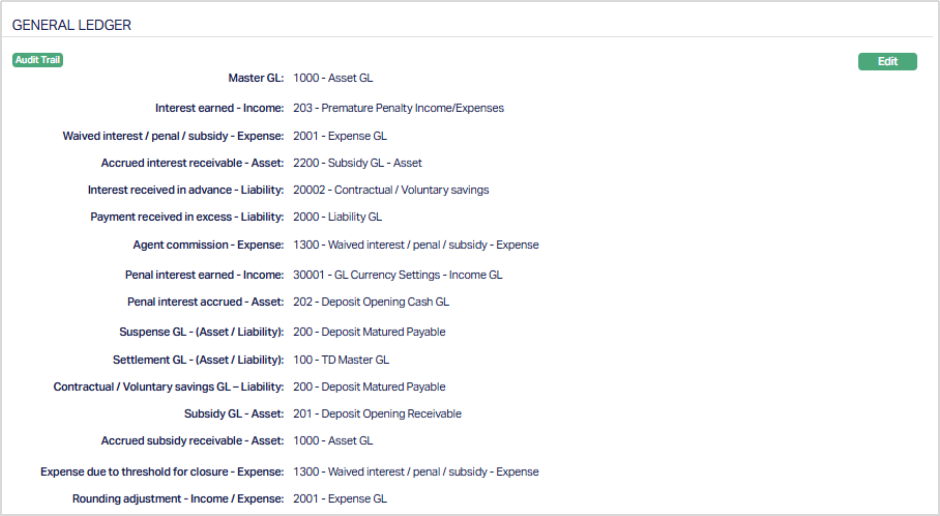

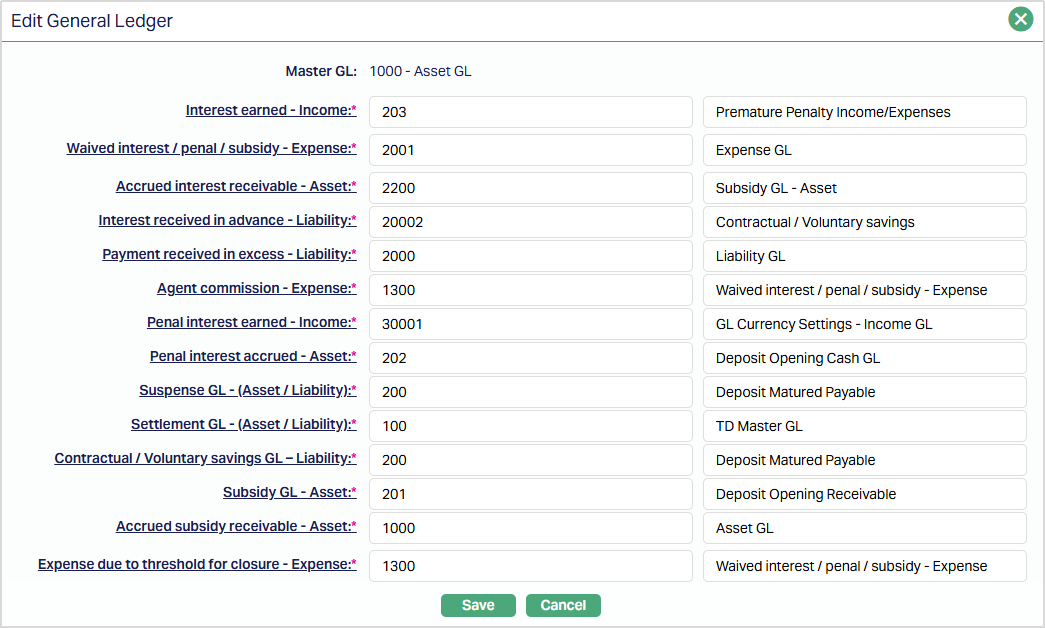

57. Click Next. The New Product → General Ledger (6/10) page appears.

58. You will see the list of various GLs required to account for the events in the life cycle of the loans under this Product. The table below gives the fields, the use and the conditions for each of these GLs. You can either directly input the Ledger # or click on the hyperlink to see the list of GLs satisfying these conditions and select the required Ledger #.

Field Details

| Sl. No. | Field name | Used | List based on |

|---|---|---|---|

| 1 | Master GL | as the Master GL to record all transactions of all accounts under this Product | ledger type Asset where Status is Active, Cash Account is No, Manual Posting is No and the FX Consolidation is blank |

| 2 | Interest earned – Income | for accounting the Interest earned on accounts under this Product | Ledger type Income where Status is Active |

| 3 | Waived interest / Penal / Subsidy Expense | for accounting the expenses on Waiver of interest / penalty / subsidy on accounts under this Product | Ledger type Expense where Status is Active |

| 4 | Accrued Interest Receivable – Asset | for accounting the Accrued interest receivable on accounts under this Product | Ledger type Asset where Status is Active |

| 5 | Interest Received in Advance - Liability | for accounting the interest received in advance on accounts under this Product | Ledger type Liability where Status is Active |

| 6 | Payment received in excess - Liability | for accounting any payments that are received in excess for accounts under this Product | Ledger type Liability where Status is Active |

| 7 | Agent commission – Expense | for accounting the Agent commission expenses on accounts under this Product. | Ledger type Expense where Status is Active |

| 8 | Penal interest earned – Income | for accounting the Penal interest earned on accounts under this Product. | Ledger type Income where Status is Active |

| 9 | Penal interest accrued – Asset | for accounting the Penal interest accrued on accounts under this Product. | Ledger type Asset where Status is Active |

| 10 | Suspense GL – (Asset / Liability) | for accounting the disbursement to external bank account for accounts under this Product | Ledger type Asset or Liability where Status is Active |

| 11 | Settlement GL – (Asset / Liability) | for accounting the disbursement / repayment through the Settlement GL, say, for cash transactions (cash disbursement or cash payments) on accounts under this Product. | Ledger type Asset or Liability where Status is Active |

| 12 | Contractual / Voluntary Savings GL - Liability | For accounting the Contractual / Voluntary savings, if Repayment is through Settlement GL for accounts under this Product. | Ledger type Liability where Status is Active |

| 13 | Subsidy GL - Asset | for accounting the interest on subsidy for accounts under this Product when the subsidy type is Claim by bank. | Ledger type Asset where Status is Active |

| 14 | Accrued subsidy receivable - Asset | for accounting the subsidy Accrued on accounts under this Product when the subsidy type is Claim by customer. | Ledger type Asset where Status is Active |

| 15 | Expense due to threshold for closure - Expense | for accounting the expenses due to threshold for closure of accounts under this Product. | Ledger type Expense where Status is Active |

| 16 | Rounding adjustment - Income/Expense | for accounting the rounding amounts during payments against invoices for accounts under this Product. | Ledger type Income or Expense where Status is Active |

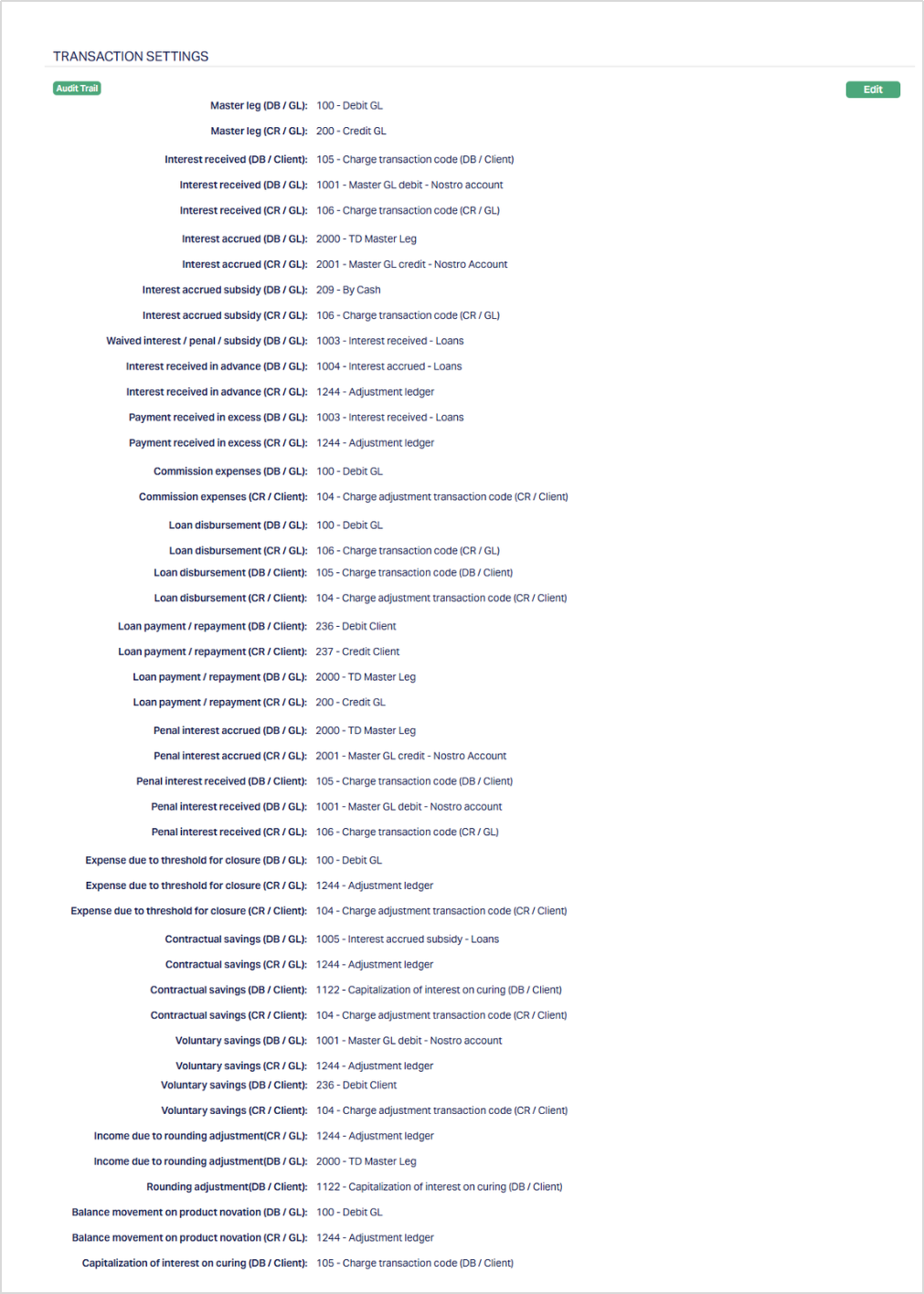

59. Click Next. The New Product → Transaction Settings (7/10) page appears.

60. Input the required Transaction codes to be used for accounting the various events in the life cycle of the loans under this Product. You can directly input the Transaction Code or use the hyperlink to search for and select the required Transaction Code. The list of Transaction codes shown on click of hyperlink is based on certain conditions as listed against each field.

| Sl. No. | Field name of Transaction Settings | Used for | List of Transaction codes based on | Event when it will be used |

|---|---|---|---|---|

| 1 | Master leg (DB/GL) | recording all the debit transactions related to Principal affecting the accounts under this Product | General Ledger Debit where Status is Active | Disbursement and Payments |

| 2 | Master leg (CR/GL) | recording all the credit transactions related to Principal affecting the accounts under this Product. | General Ledger Credit where Status is Active | Disbursement and Payments |

| 3 | Interest received (DB/Client) | recording all Interest received in the Client Account. | Client account Debit where Status is Active | Payments |

| 4 | Interest received (DB/GL) | recording all Interest received debit transactions in the General Ledger Account. | General Ledger Debit where Status is Active | Payments |

| 5 | Interest received (CR/GL) | recording all Interest received credit transactions in the General Ledger Account. | General Ledger Credit where Status is Active | Payments |

| 6 | Payment received in excess (DB/GL) | recording all excess payment debit transactions in the General Ledger Account. | General ledger Debit where Status is Active | Payments |

| 7 | Payment received in excess (CR/GL) | recording all excess payment credit transactions in the General Ledger Account. | General ledger Credit where Status is Active | Payments |

| 8 | Interest accrued (DB/GL) | recording all Interest accrued debit transactions in the General Ledger account. | General ledger Debit where Status is Active | Accrual |

| 9 | Interest accrued (CR/GL) | recording all Interest accrued credit transactions in the General Ledger account. | General ledger Credit where Status is Active | Accrual |

| 10 | Interest accrued subsidy (DB/GL) | recording all the Debit transactions for the subsidy on interest accrual in the General Ledger account. | General ledger Debit where Status is Active | Accrual |

| 11 | Interest accrued subsidy (CR/GL) | recording all the Credit transactions for the subsidy on interest accrual in the General Ledger account. | General ledger Credit where Status is Active | Accrual |

| 12 | Waived interest / Penal / Subsidy (DB/GL) | recording all Penal / Subsidy / Interest waived transactions in the General Ledger account. | General ledger Debit where Status is Active | Accrual, Payments |

| 13 | Interest received in advanced (DB/GL) | recording all debit transactions on interest received in advance in the General Ledger account. | General ledger Debit where Status is Active | Payments |

| 14 | Interest received in advanced (CR/GL) | recording all credit transactions of the interest received in advance in the General Ledger account. | General ledger Credit where Status is Active | Payments |

| 15 | Commission expenses (DB/GL) | recording all commission expense transactions in the General Ledger account. | General ledger Debit where Status is Active | - |

| 16 | Commission expenses (CR/Client) | recording all commission expense transactions in the Client account. | Client account Credit where Status is Active | - |

| 17 | Loan disbursement (DB/GL) | recording all loan disbursement debit transactions in the General Ledger accounts. | General ledger Debit where Status is Active | Disbursement |

| 18 | Loan disbursement (CR/GL) | recording all loan disbursement credit transactions in the General Ledger accounts. | General ledger Credit where Status is Active | Disbursement |

| 19 | Loan disbursement (DB/Client) | for recording all loan disbursement debit transactions in the Client accounts. | Client account Debit where Status is Active | Disbursement |

| 20 | Loan disbursement (CR/Client) | for recording all loan disbursement credit transactions in the Client accounts. | Client account Credit where Status is Active | Disbursement |

| 21 | Loan payment/repayment (DB/Client) | for recording all payment / repayment debit transactions in the Client account. | Client account Debit where Status is Active | Payment/Repayment |

| 22 | Loan payment/repayment (CR/Client) | for recording all payment / repayment credit transactions in the Client account. | Client Account Credit where Status is Active | Payment/Repayment |

| 23 | Loan payment/repayment (DB/GL) | recording all payment / repayment debit transactions in the General Ledger account. | General Ledger Debit where Status is Active | Payment/Repayment |

| 24 | Loan payment/repayment (CR/GL) | recording all payment / repayment credit transactions in the General Ledger account. | General Ledger Credit where Status is Active | Payment/Repayment |

| 25 | Penal interest accrued (DB/GL) | for recording the debit transactions in the General Ledger account in respect of the Penal Interest Accrued. | General Ledger Debit where Status is Active | Accrual |

| 26 | Penal interest accrued (CR/GL) | for recording the credit transactions in the General Ledger account in respect of the Penal Interest Accrued. | General Ledger Credit where Status is Active | Accrual |

| 27 | Penal interest received (DB/Client) | for recording the debit transactions in the Client account in respect of the Penal Interest Received. | Client account Debit where Status is Active | Payment |

| 28 | Penal interest received (DB/GL) | for recording the debit transactions in the General Ledger account in respect of the Penal Interest Received. | General Ledger Debit where Status is Active | Payment |

| 29 | Penal interest received (CR/GL) | for recording the credit transactions in the General Ledger account in respect of the Penal Interest Received. | General Ledger Credit where Status is Active | Payment |

| 30 | Expense due to threshold for closure (DB / GL) | for recording the debit transactions in the General Ledger account in respect of the Expense due to threshold for closure. | General Ledger Debit where Status is Active | Payment, Closure |

| 31 | Expense due to threshold for closure (CR / GL) | for recording the credit transactions in the General Ledger account in respect of the Expense due to threshold for closure. | General Ledger Credit where Status is Active | Payment, Closure |

| 32 | Expense due to threshold for closure (CR / Client) | for recording the credit transactions in the Client account in respect of the Expense due to threshold for closure. | Client account Credit where Status is Active | Payment, Closure |

| 33 | Contractual savings (DB/GL) | For recording the contractual savings debit transactions in the GL. | General Ledger Debit where Status is Active | Payment |

| 34 | Contractual savings (CR/GL) | For recording the contractual savings GL transactions if the repayment is done through Settlement GL. | General Ledger Credit where Status is Active | Payment |

| 35 | Contractual savings (DB/Client) | For recording the contractual savings debit transactions to the Client account. | Client account Debit where Status is Active | Payment |

| 36 | Contractual Savings (CR/Client) | For recording the contractual savings credit transactions to the Client account. | Client account Credit where Status is Active | Payment |

| 37 | Voluntary savings (DB/GL) | For recording the voluntary savings debit transactions in the GL. | General Ledger Debit where Status is Active | Payment |

| 38 | Voluntary savings (CR/GL) | For recording the voluntary savings GL transactions if the repayment is done through Settlement GL. | General Ledger Credit where Status is Active | Payment |

| 39 | Voluntary savings (DB/Client) | For recording the voluntary savings debit transactions to the Client account. | Client account Debit where Status is Active | Payment |

| 40 | Voluntary savings (CR/Client) | For recording the voluntary savings credit transactions to the Client account. | Client account Credit where Status is Active | Payment |

| 41 | Income due to rounding adjustment (CR/GL) | for accounting the credit transactions to the GL due to rounding amounts. | General Ledger Credit where Status is Active | Payment |

| 41 | Income due to rounding adjustment (DB/GL) | for accounting the debit transactions to the GL due to rounding amounts. | General Ledger Debit where Status is Active | Payment |

| 42 | Rounding adjustment (DB/Client) | for accounting the debit transactions to the Client account due to rounding amounts. | Client account Debit where Status is Active | Payment |

| 43 | Balance movement on Product novation (DB/GL) | for accounting the debit transactions to the General Ledger account due to balances to be moved on Product Novation | General Ledger Debit where Status is Active | Product Novation |

| 44 | Balance movement on Product novation (CR/GL) | for accounting the credit transactions to the General Ledger account due to balances to be moved on Product Novation | General Ledger Credit where Status is Active | Product Novation |

| 45 | Capitalization of interest on curing (DB/Client) | for accounting the capitalization of the interest amount earmarked for curing under a Payment Plan | Client account Debit where Status is Active | Payment Plan |

61. Click Next. The New Product → Statement Parameter (8/10) page appears.

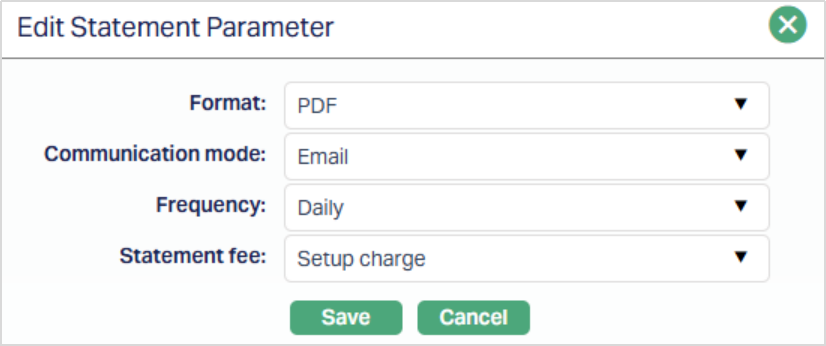

62. Select Format from the drop-down list of statement formats that have been maintained under Admin → System codes → Generic definition → Statement formats. It is the format of the statement that is to be generated.

63. Select Communication mode i.e., the manner in which you want to send the statement from the drop down. Available options are Data handoff, e-Invoice, Email, Paper, SMS and Web hotel.

64. Select Frequency of the statement to be generated from the drop down. Available options are: Daily, Weekly, Fortnightly, Monthly, Quarterly, Semi-annual and Annual.

65. Select the Statement fee from drop down list of all Active charges maintained under Admin → Pricing → Charges where the Charge Type is Event, it is not a Deferred Charge, Treat as Commission = No, Treat as Receivable = No and Amortization = No. If the Charge is Banded, the charge amount will be calculated on the basis of the amount sanctioned. If a Charge account is attached to the loan account, then the charge amount is debited from the charge account on statement generation; else, it is created as a charge schedule with due date same as upcoming Principal / Interest / Annuity schedule due date.

66. Click Next. The New Product → Custom Field (9/10) page appears.

Note: Only if any custom field is mapped to Mortgage and Loan Product under Admin → System Codes → Custom fields → Field mapping, the additional screen will appear before the confirmation screen as shown above; else, the same will not be displayed. The custom fields will be mandatory or non-mandatory based on the rules set at the Field mappings. For more details on custom field functionality please refer Admin → System codes → Custom fields → Field mappings manual.

67. Enter the details as required and Click Next. The New Product → Confirmation (10/10) page appears showing all the details that you entered above.

68. Click Finish. The new Product record is created, and you will see the Profile tab by default.

Note: The Status of the Product is Active as soon as the Product is created. The status of the Interest Receivable tab, Special Interest Scheme, Charge tab and Statement Parameter will be Pending till it is approved by another user as indicated by the red bubble on the tab. On approval, the tab status is set to Approved. If the tab status is Pending, loan accounts under the Product cannot be created.

Edit: Using Edit, you can update certain details of the Product. However, the updated conditions will be applicable only for any accounts that are created AFTER the changes have been done and will NOT affect the accounts already created.

Suspend: You can suspend the Product by a click on Suspend button. When you click on Suspend button, Aura displays an alert message. On confirmation Aura will suspend the Product. Suspending a Product only makes it unavailable in future for any new account creation / any other dropdown list. Existing accounts under the Product continue without any impact. Suspended Products can be activated by using Activate button.

Activate: You can activate a suspended Product by a click on Activate button. When you click on Activate button, Aura displays an alert message. On confirmation Aura will activate the Product. Activation of a Product makes it available in future for any new account creation / any other dropdown list.

Profile

The Profile tab, which is the default tab in the Product screen, shows the basic details of the Product.

To view / edit Profile.

1. Access Product page and retrieve the required Product record using Search. Click Profile tab to view the details as per sample below. The details are defaulted from the entries that you made during Product creation. For details refer to Mortgage and Loan > New Product → Profile (1/10).

2. Click Edit. Edit Product page appears.

The following fields are editable:

Description

Available for: You can only add the client types. But you cannot remove a client type for which the Product was marked as available earlier.

3. Click Save. Profile page appears with the edited details.

Functions: Edit

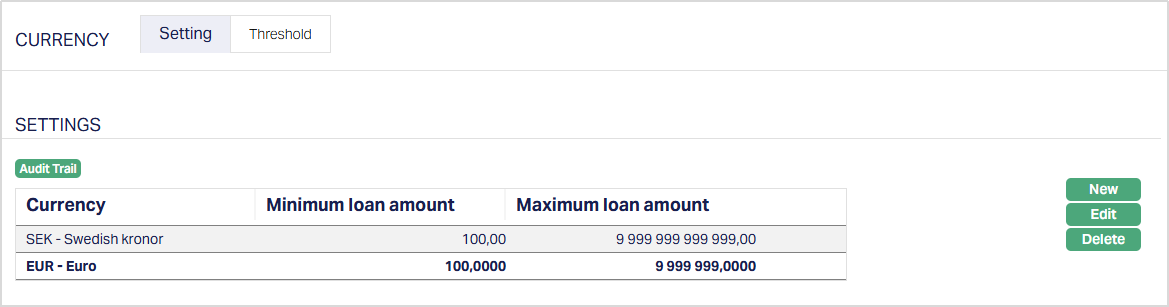

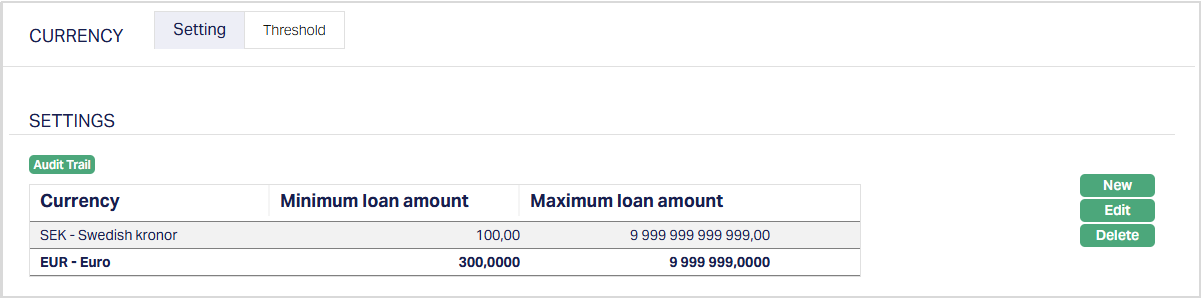

Currency

The Currency tab allows you to maintain the currencies for the Product. One or more currencies can be added using the Currency tab, once the Product record is created. Accounts for the Product can be opened only in the selected currencies. You can also maintain the threshold parameters for each currency

The sub-tabs available under this tab are

Setting

Using the Settings sub-tab, you can add / remove currencies and update the amount range for each currency for loans under a Product.

To add a currency,

1. Access the Product Maintenance page and retrieve the required Product record using Search.

2. Click on the Currency tab to view the details as per sample shown below under sub tab Settings. The details are defaulted from the entries that you made during Product creation / last edit. For details refer to Mortgage and Loan → New Product → Currency (2/10).

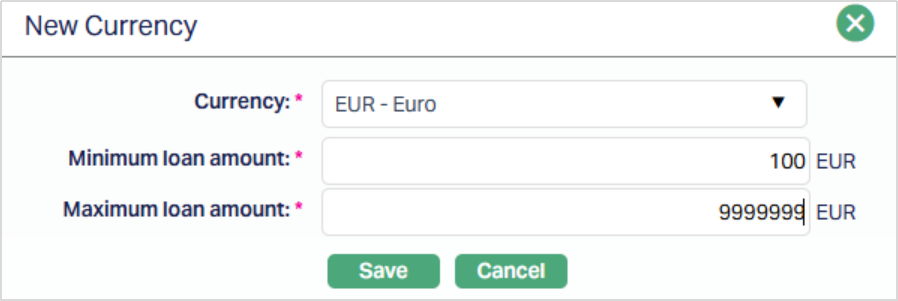

3. Click New. The New Currency page will appear.

4. Select the Currency that you would like to add under the Product from the drop-down list of GL currencies maintained under General Ledger → Settings → Currency.

5. Enter the Minimum loan amount for the loan accounts under the Product for this currency.

6. Enter the Maximum loan amount for the loan accounts under the Product for this currency. Maximum amount should be greater than the minimum amount.

7. Click Save. The Currency tab appears with the added new currency added under the sub-tab Settings.

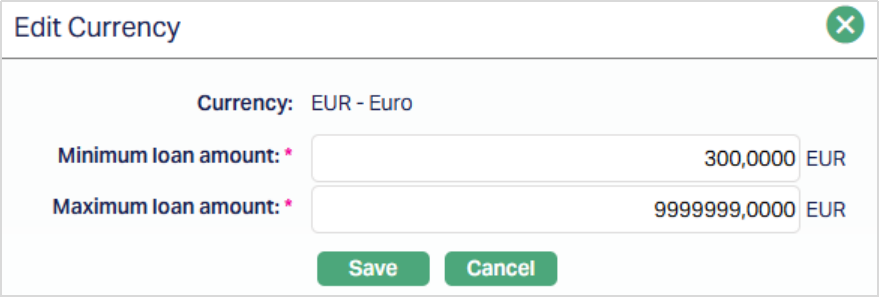

To edit the minimum / maximum loan amounts allowed for the Product under each currency

1. Click Edit. The Edit Currency page appears.

Note: The editable fields are Minimum Loan Amount and Maximum Loan Amount.

2. Input the required details and click Save. The Currency tab appears with the edited details under the sub-tab Settings.

Functions: New, Edit and Delete.

Delete: You can delete a currency by clicking on the Delete button. When you click on the Delete button, Aura displays an alert message. On confirmation, Aura will delete the currency, only if there are no Loan Accounts already created under the Product. Also, a Product must support at least one currency; and hence, if there is only one currency defined for the Product, it cannot be deleted.

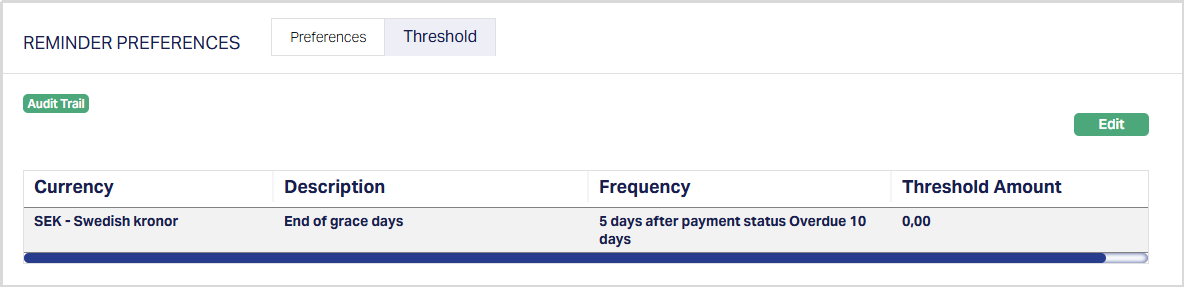

Threshold

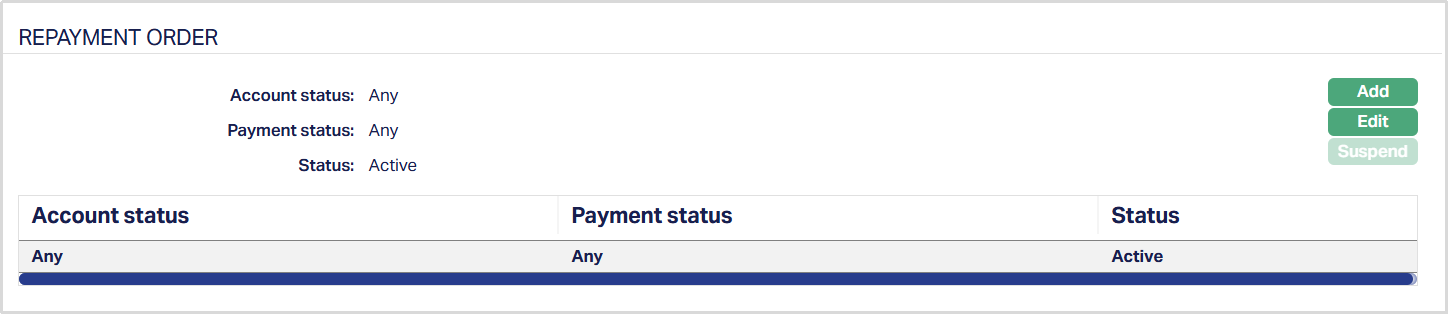

The Threshold sub-tab allows you to maintain the values for thresholds applicable to the Product for each currency. These thresholds control how Aura processes receipts, prepayments, overdues and excess amounts under different conditions.

When a Currency is added to the Product in the Add Wizard or in the Currency → Settings sub-tab, a Threshold record is automatically created with the Amount = 0.00. You can then edit the record to maintain the required threshold values.

To view the details of Threshold sub-tab,

1. Access Product Maintenance page. Click on the Currency tab and then click on Threshold sub-tab to view the details as per sample below

Function: Edit

The following Thresholds are available in this sub-tab:

1. Ceiling for Maximum Prepayment or Excess Receipts - This threshold defines the maximum amount that can be accepted as Prepayment or Excess Receipts.

- If the excess amount after allocation to dues exceeds this ceiling, Aura rejects the payment with an error message.

- By default, this field is set to maximum allowable system value, but you can revise as required.

- The Ceiling is applied in both cases:

- If Treat Excess Receipts = Prepayment → payment fails if it exceeds the ceiling.

- If Treat Excess Receipts = Received In Excess → payment fails if it exceeds the ceiling. Any transaction breaching this ceiling requires manual intervention

2. Threshold for Minimum Prepayment - This threshold defines the minimum amount required for treating excess receipts as Prepayment.

- If the excess amount after allocation to dues is greater than or equal to this threshold, Aura classifies it as Prepayment, if Treat Excess Receipts = Prepayment.

- If the excess amount is less than this threshold, it is treated as Received in Excess (RIE) even if Treat Excess Receipts = Prepayment.

3. Threshold for Overdue Days - This threshold defines the amount after which the loan is considered as overdue such that for small amounts (say < 10 EUR), the loan is not treated as an Overdue Loan.

Example:

Threshold for Overdue Days = 70.00 EUR

Penalty on Principal Overdue = 24%

Loan Account Schedule

| Schedule Due Date | Component | Due Amount | Paid Amount | Unpaid Amount |

|---|---|---|---|---|

| 26-Sep-2024 | Principal | 50.00 | 0.00 | 50.00 |

| 26-Sep-2024 | Interest | 10.00 | 0.00 | 10.00 |

| 26-Sep-2024 | Instalment fee | 12.00 | 2.00 | 10.00 |

Assuming Grace Days = 1, on 27-Sep-2024, Penalties will be applied on the Principal and Interest overdue amounts and the Schedule will be as follows:

| Schedule Due Date | Component | Due Amount | Paid Amount | Unpaid Amount |

|---|---|---|---|---|

| 26-Sep-2024 | Principal | 50.00 | 0.00 | 50.00 |

| 26-Sep-2024 | Interest | 10.00 | 0.00 | 10.00 |

| 26-Sep-2024 | Instalment fee | 12.00 | 2.00 | 10.00 |

| 26-Sep-2024 | Penalty on Principal Overdue | 0.06 | 0.00 | 0.06 |

For purposes of calculating the overdue days, the Overdue Amount as on 27-Sep-24 on the above account will be arrived at by summing up all the unpaid amounts except the Penalty components and compared with the Threshold defined. When the sum of such unpaid amounts exceeds the Threshold, it will be considered to be Overdue. In the above case, the total Overdue Amount = Sum of unpaid amounts of Principal, Interest and Instalment Fee = 70.00 which is equal to the Threshold for Overdue Days. Hence, the loan will NOT be considered to be overdue for purposes of Status Movement as per the Status Rules defined for the Product. The number of overdue days will be considered as 0

However, if there was no payment received towards the Instalment Fee, the toal of Unpaid Amount would be 72.00 which is > Threshold for Overdue Amount; and hence, the Loan will be considered as Overdue from the Due Date i.e., 26-Sep-2024; and Overdue Days would be calculated as Current Booking Date minus Overdue Since Date.

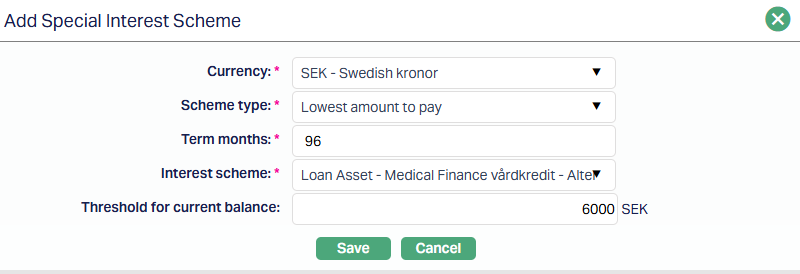

4. Threshold for Movement to Lowest Amount - This threshold applies only to a Product where Apply Special Interest Scheme = Yes. It defines the maximum overdue amount allowed before the movement into the Lowest Amount to Pay category. When this threshold is breached, the concessional interest rate no longer applies, and the .normal interest rate becomes effective

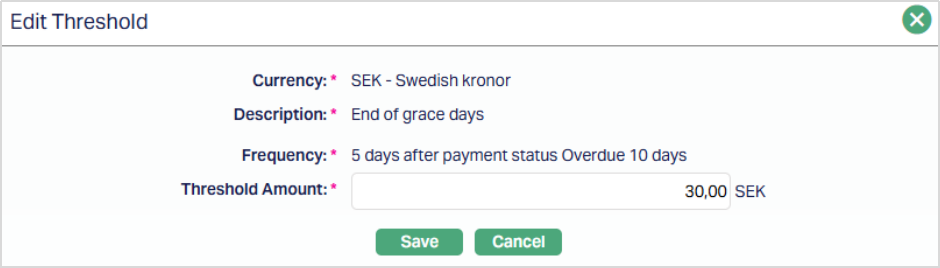

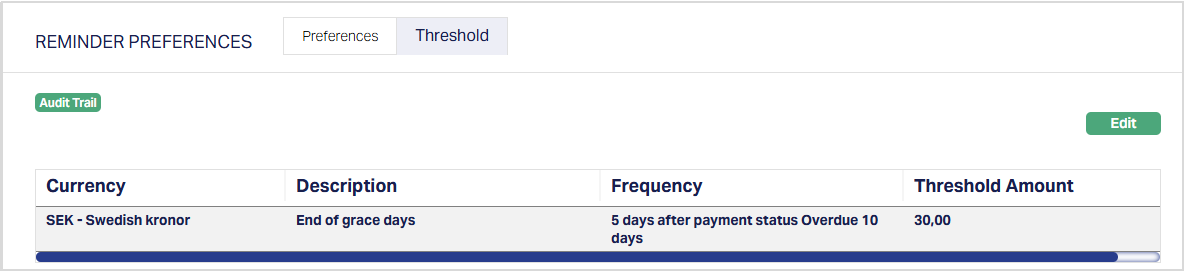

To edit Threshold,

1. Access Product Maintenance page. Click on the Currency tab and then click on Threshold sub-tab

2. Select the required Threshold record and click Edit. The Edit Threshold page for that currency will appear.

Only the Threshold amount field is editable.

3. Update the amount as required.

4. Click Save. The Threshold sub-tab appears with the edited details.

Function: Edit

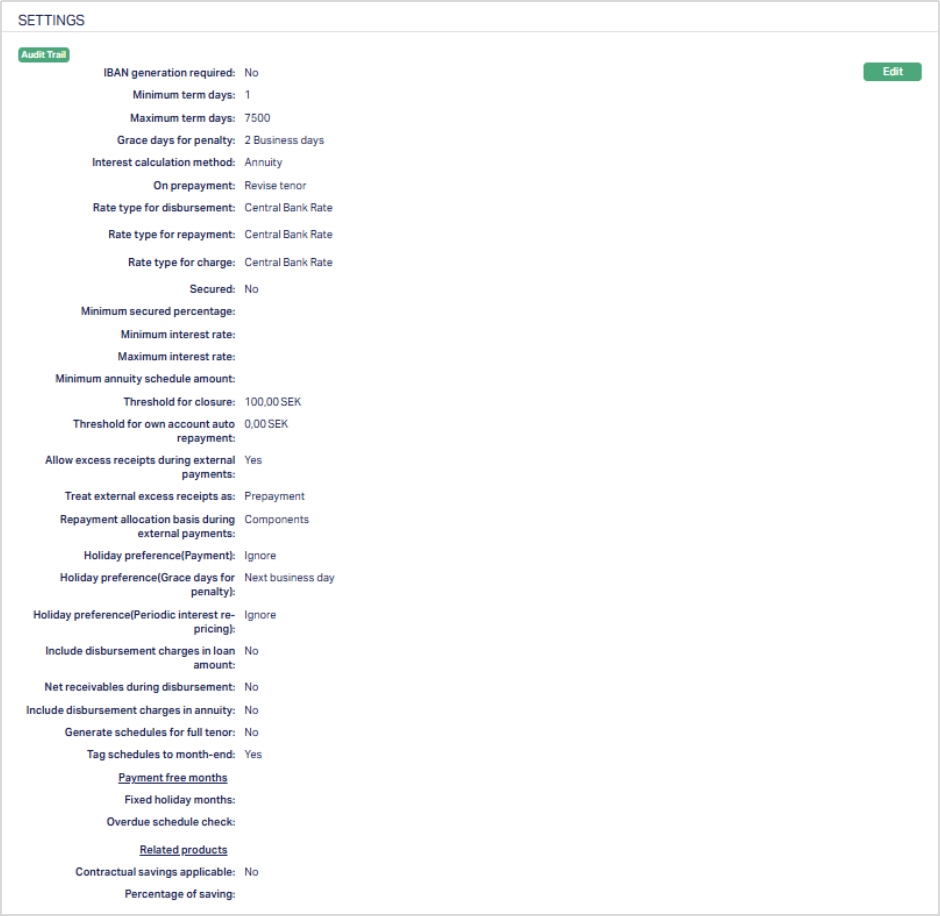

Settings

This Tab allows you to view and maintain certain Product settings like IBAN generation required, Minimum and maximum term days, Rate types for currency conversions, holiday preferences, payment free months, parameters related to repayment, etc.

To edit the settings,

1. Access Product Maintenance page. Click Settings tab to view the details as per sample below. The details are defaulted from the entries that you made during Product creation. For details refer to Mortgage and Loan → New Product → Settings (3/10).

2. Click Edit. The Edit Product Settings page appears.

Note: All fields in the Edit Product Settings page are editable except the Interest Calculation method.

Additional fields available here are:

1. Allow Excess Receipts during External Payments: By default, this field is set to No to ensure that the amount received from the borrower through an external bank does not exceed the total amount due on the Loan Account or Invoice. If you wish to allow borrowers to pay more than the due amount and have Aura automatically process the excess either as a Principal Prepayment or as Amount Received in Excess, select Yes.

When enabled, the received amount is first adjusted against all amounts due, and any surplus is treated as a prepayment towards the Principal Outstanding or as Amount Received in Excess. See note below the next point for more details.

2. Treat External Excess Receipt as: This field becomes editable only when Allow Excess Receipts during External Payments is set to Yes. You can select one of the following options -

- Prepayment - Excess receipts will be applied toward the Principal Prepayment.

- Received in Excess - Excess receipts will be recorded separately without affecting the principal balance.

Note: External Payment Processing with reference to Excess Receipts

When an external payment is received in Aura:

a. Allocation to dues →

- Aura first applies the payment against outstanding dues for the invoice / loan account based on payment reference received as invoice # or loan account # respectively.

b. Check Minimum Prepayment Threshold →

- If the excess amount remaining after allocation to dues is greater than or equal to Minimum Prepayment Threshold, it is treated as Prepayment, provided Allow Excess Receipts during External Payments = Yes and Treat External Excess Receipts As = Prepayment.

- If the excess amount is lesser than the Minimum Prepayment Threshold, it is treated as Received in Excess (RIE), provided Allow Excess Receipts during External Payments = Yes, irrespective of where Treat External Excess Receipts As = Prepayment or Received in Excess; else, Aura rejects the payment with an error message.

c. Check Maximum Ceiling →

- If the excess amount (whether Prepayment or RIE) exceeds the Maximum Ceiling, Aura rejects the payment with an error message. Such transactions require manual intervention to proceed.

These layered validations ensure that the receipts are classified consistently and do not breach the limits defined for the Product.

3. Repayment Allocation Basis during External Payments - This field gives you an ability to define how repaid amounts should be allocated when the Payment Reference in an External Payment is the Loan Account. The options available are:

- Components - This is the default option when the Product record is created. Allocation is done component-wise (as per Repayment Order) across all unpaid schedules, starting from the oldest schedule. Once a component is fully allocated across all schedules, the next component in the repayment order is processed.

- Schedule due dates - Allocation is performed schedule-wise. The payment is applied first to the oldest schedule across all components (following the Repayment Order). Once all components within that schedule are settled, allocation moves to the next oldest schedule.

Notes:

- When Schedule Due Dates is selected, penalty allocation is determined based on the Unpaid Amount in the schedule, not the Invoiced Amount. Therefore, if multiple schedules are overdue, Aura allocates payments starting with the oldest schedule, applying payments to each component in order. The penalty allocation may therefore exceed the invoiced penalty amount, as it is based on unpaid amounts Aat the time of allocation, rather than invoiced amounts.

- If the Payment Reference in the external payment is Invoice Number, amounts are allocated on the basis of Components as per the Repayment Order defined in the Product.

4. Tag Schedules to Month-end: This field determines how Aura generates future repayment schedules when the first or next installment date falls on the last day of a month (for example, 28-Feb in a non-leap year). By default, this flag is checked when the Product is created and can be edited during Edit → Settings. Any change made here will apply only to Loan Accounts created after the change.

When a Loan Account is created, the value of this flag is automatically defaulted from the Product internally. It is not displayed in the Loan Account UI and therefore cannot be modified at the account level.

During schedule generation or regeneration, when the first or next payment date falls on a month-end, and if the Principal/ Interest / Annuity Frequency is set as Monthly, Quarterly, Semi-Annual, or Annual, Aura checks the value of this flag:

- If this flag is checked, the subsequent schedules are generated using month-end dates

- If this flag is unchecked, schedules are generated using the same date (DD part of the DD-MM-YYYY) as the first or next payment date instead of month-end.

Examples:

| First / Next Payment Date | Is it a month-end date? | Flag considered? | Flag Value | Subsequent Schedule Dates |

|---|---|---|---|---|

| 28th Feb of a non-leap year | Yes | Yes | Checked | 31st Mar, 30th Apr, 31st May and so on |

| 28th Feb of a leap year | No | No | Checked | 28th Mar, 28th Apr, 28th May, 28th Jun and so on |

| 29th Feb of a leap year | Yes | Yes | Checked | 31st Mar, 30th Apr, 31st May and so on |

| 30th Nov | Yes | Yes | Checked | 31st Dec, 31st Jan, 28th Feb (or 29th Feb in case of a leap year, as Feb does not have 30 days), 31st Mar, 30th Apr and so on |

| 30th Dec | No | No | Checked | 30th Jan, 28th Feb (or 29th Feb in case of a leap year, as Feb does not have 30 days), 30th Mar, 30th Apr and so on |

| 15th Dec | No | No | Checked | 15th Jan, 15th Feb, 15th Mar, 15th Apr and so on |

| 28th Feb of a non-leap year | Yes | Yes | Unchecked | 28th Mar, 28th Apr, 28th May and so on |

| 28th Feb of a leap year | No | No | Unchecked | 28th Mar, 28th Apr, 28th May, 28th Jun and so on |

| 29th Feb of a leap year | Yes | Yes | Unchecked | 29th Mar, 29th Apr, 29th May and so on |

| 30th Nov | Yes | Yes | Unchecked | 30th Dec, 30th Jan, 28th Feb (or 29th Feb in case of a leap year, as Feb does not have 30 days), 30th Mar, 30th Apr and so on |

| 30th Dec | No | No | Unchecked | 30th Jan, 28th Feb (or 29th Feb in case of a leap year, as Feb does not have 30 days), 30th Mar, 30th Apr and so on |

| 15th Dec | No | No | Unchecked | 15th Jan, 15th Feb, 15th Mar, 15th Apr and so on |

5. Payment-Free Months: Aura enables you to grant Payment Free Month(s) by selecting specific months in the Fixed Holiday Months field. If installments are due during a Payment-Free Month, they are treated as zero, and the subsequent instalment includes the cumulative Principal, Interest, and Charges.

This option is not applicable in the month of Maturity Date.

6. Overdue Schedule Check determines eligibility for Payment-Free Month applicability. The following options are available:

- No check - If you want to specify that the payment free month is applicable irrespective of whether the account is overdue or not, choose this option. No overdue status check for the account will be performed.

- Check overdue for X cycles - If you want to specify that the payment free month is applicable only if the account has not been overdue for the past X cycles, choose this option. Aura will check if the account has gone overdue for the past X cycles and if so, disallow the Payment Free Months.

7. Contractual Savings applicable is a long-term savings involving a definite, continuous commitment on the part of the savers; and is usually combined with a micro-finance loan to encourage the borrowers to save along with repayment of the loans. If you are creating a Product where there should be compulsory savings along with repayment, Select the radio button Yes or No as required.

Note: If you select Yes then the Percentage of Savings field is enabled for you to input.

8. Percentage of Savings is enabled when you have chosen Contractual Savings = Yes in the above field. Enter the percentage of saving as required. The total contractual savings for the loan will be calculated as a % of the Loan Approved amountand will be amortized over the period of the loan, based on the number of principal payments.

9. Click Save. The Settings page appears with the edited details.

Function: Edit

Availability

This tab can be used to control the availability of the Product to specific Branch, Offering Category or Client. It has three sub-tabs, one for each of these.

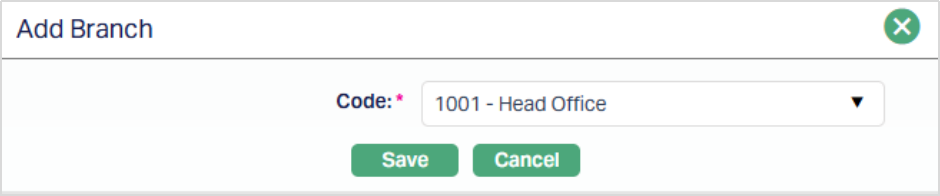

Availability-Branch

Using this tab, you can allow the Product to be available for all the branches or only specific branch(es).

To select the required branch,

1. Go to Product page, click on Availability tab, then click on Branch tab.

2. By default, All radio button is selected so that this Product is available for all Branches.

3. To restrict the branches for which this Product is available, click Selected radio button. Add button is now enabled.

4. Click Add. The Add Branch screen appears where you can select the required branch from the drop down of all active branches of the Entity maintained under Admin → Branches → Maintain

5. Click Save. The Availability tab appears with the added branch details under Branch Sub tab.

Function: Add, Delete

To delete a branch, select the branch and click Delete.

Note: You may choose to allow All branches for the Product at any time. However, Aura will prompt you to confirm if the selected Branches may be deleted. If confirmed, then all the selected Branches will be deleted, and the Product will be available for ALL branches.

Availability-Offering

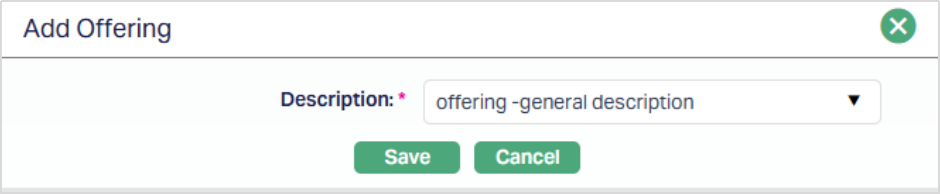

Using this tab, you can allow the Product to be available for all the Offering Categories or only specific Offering Categories.

1. Go to Product page, click on Availability tab, then click on Offering tab.

2. By default, All radio button is selected so that this Product is available for all Offerings.

3. To restrict the Offerings that are available under this Product, click on Selected radio button. Add button is now enabled.

4. Click on Add. Add Offering screen appears where you can select the required Offering from the drop-down list of active Offerings maintained under Admin → System Codes → Categories → Offering

5. Click Save. The Availability tab appears with the added offering details under Offering Sub tab.

Function: Add, Delete

NOTE: You may choose to allow All Offerings for the Product at any time. However, Aura will prompt you to confirm if the selected Offering Categories may be deleted. If confirmed, then all the selected Offering Categories will be deleted, and the Product will be available for ALL Offering Categories.

Availability-Client

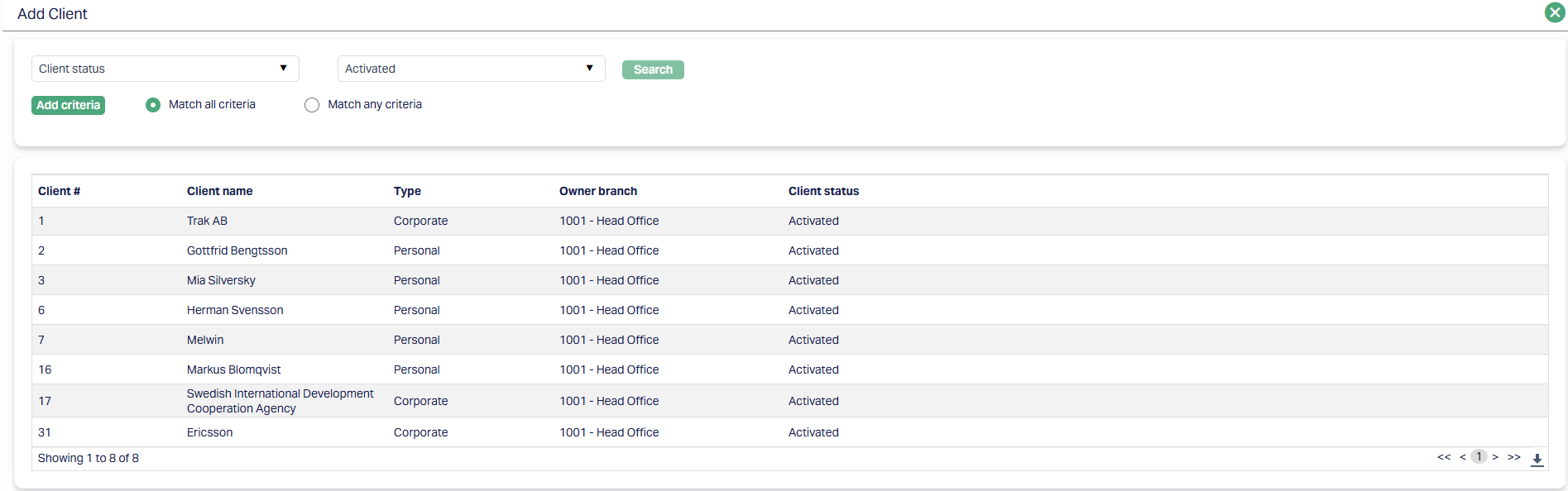

Using this tab, you can allow the Product to be available for all the Clients or only specific Client(s).

1. Go to Product page, click on Availability tab, then click on Client tab.

2. By default, All radio button is selected so that this Product is available for all Clients.

3. To restrict the Clients for which this Product is available, click Selected radio button. Add button is now enabled.

4. Click Add. The Add Client page appears, where you can search for the required client with relevant criteria and select the required client

5. The Availability tab appears with the added Client details under Client Sub tab.

Function: Add, Delete

To delete a client, select the client and click Delete.

Note: You may choose to allow All clients for the Product at any time. However, Aura will prompt you to confirm if the selected clients may be deleted. If confirmed, then all the selected clients will be deleted, and the Product will be available for ALL Clients.

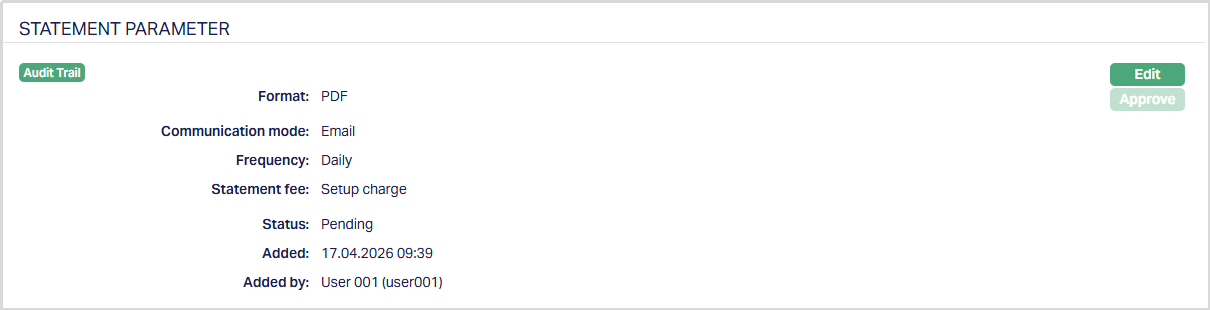

Statement Parameter

Using this tab, you can view and maintain the preferences for generating the statements.

To view/edit the Statement Parameter,

1. Access the Product page. Click on the Statement Parameter tab to view the details as per sample below. The details are defaulted from the entries that you made during Product creation / last edit. For details refer to Mortgage and Loan → New Product → Statement Parameter (8/10).

2. Click Edit. The Edit Statement Parameter page appears.

All the fields in Statement Parameter are editable.

3. Click Save. The Statement Parameter page appears with the edited details.

Note: After edit, the Status of Statement Parameter tab will reflect as Pending with a red bubble on the Tab. To approve, a user different from the one who created / edited has to retrieve the record and click Approve. Once the tab is approved the red bubble disappears and the Status changes to Approved as shown below.

Function: Edit and Approve

The additional fields that you can view in the Statement Parameter tab are explained below.

Status field denotes the status of the record.

Added field denotes the date on which the record was added.

Added by field denotes the name of the user who created the record.

Approved field denotes the date on which the record was approved and is displayed only on approval.

Approved by field denotes the name of the user who approved the record and is displayed only on approval.

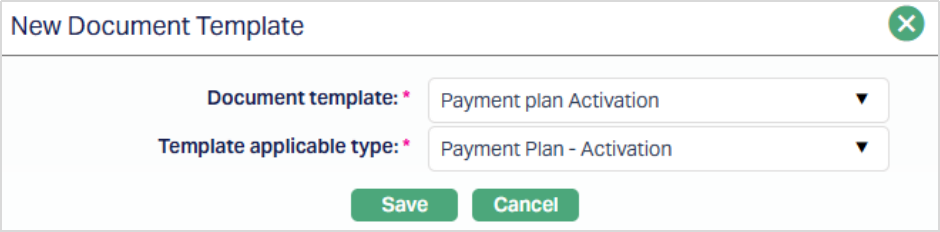

Document Template Settings

Using this tab, you can maintain the document template which can be used for creating documents for all the accounts maintained under this Mortgage and Loan Product.

Note: This feature has to be customized for each bank during implementation as per their specific requirements.

To add a new Document template settings,

1. Access the Product page. Click on the Document Template Settings tab.

2. Click New. New Document Template page appears.

3. Select the Document template from the available dropdown as maintained under Admin → System codes → Document → Document templates.

4. Select the Template applicable type from the available drop-down. The available options are:

- Disbursement

- Insurance-Cancellation

- Insurance-Initiation

- Insurance-Reactivation

- Insurance-Suspension

- Product novation

- Payment Plan-Activation

- Payment Plan-Completion

- Maintain

- Repayment

- Restructuring

- Partial Prepayment

- Full Prepayment

- Simulation of Payment

- Change of Terms-Settings

- Change of Terms-Interest Parameters

- Change of Terms-Payment Terms

- Change of Terms-Invoice Cancellation

5. Click Save. The Document Template Settings tab appears with the added details.

Functions: New and Delete.

Delete: You can delete a Document Template by clicking on the Delete button. Aura will ask for confirmation, on approving which the selected record will be deleted.

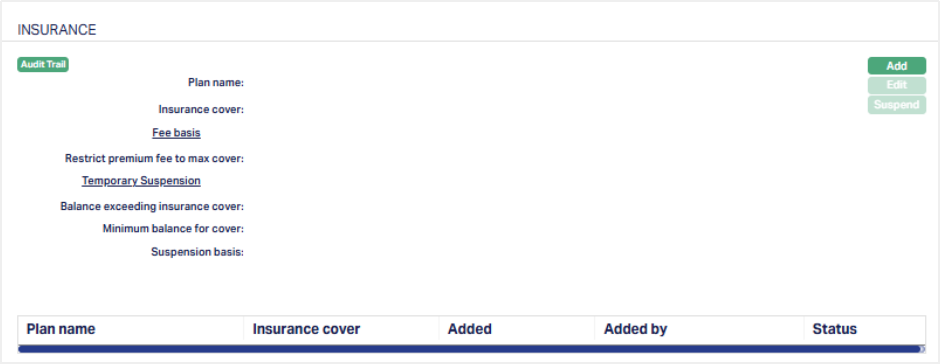

Insurance Plan

This tab allows you to map insurance plans that can be linked to the loan accounts created under the Product. You can maintain the details of the plan, such as fees, coverage limits, and suspension conditions.

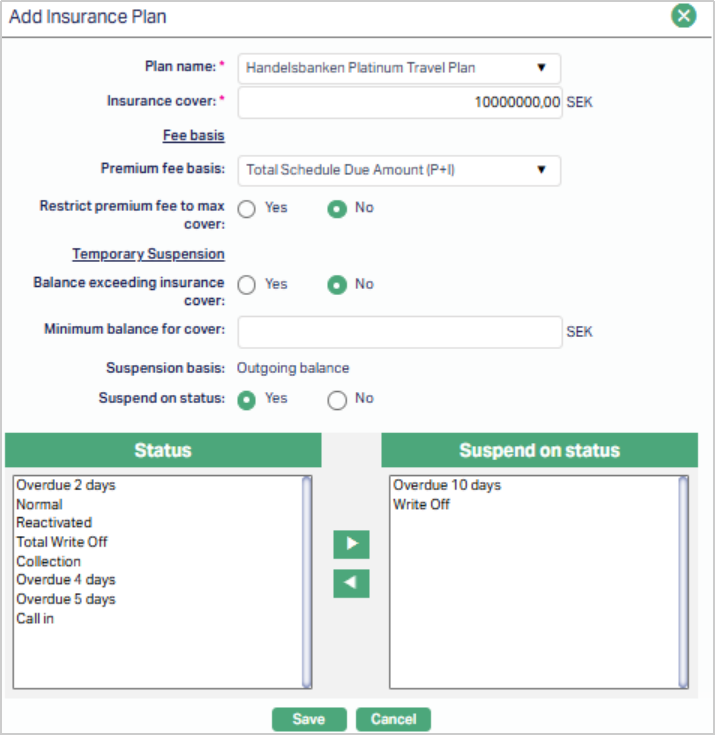

To add a new Insurance Plan,

1. Access the Product page and click on the Insurance Plan tab. On creation of Product, this tab will be blank. If any plans have already been added, these will be displayed.

2. Click Add. The Add Insurance Plan page appears.

3. Select the required Plan name from the drop-down list of insurance plans maintained as available for this specific Product or for all Products under Admin → System Codes → Generic Definitions → Insurance Plan → Availability Tab.

Note: Once an insurance plan is mapped to a Product, it cannot be added again to the same Product

4. Specify the maximum amount of Insurance cover under this plan for loan accounts created under this Product. By default, Aura displays the maximum cover defined for the plan under Admin → System Codes → Generic Definitions → Insurance Plan. The Insurance Cover value can be reduced at the Product level but cannot exceed the Maximum Cover defined under Admin → System Codes → Generic Definitions → Insurance Plan.

Under Fee Basis, you can define the following:

5. Premium fee basis defines the base used for calculating the insurance premium fee. You can choose from three available options, allowing flexibility in how the premium amount is derived:

- Outgoing Balance - Calculates the premium fee based on the current outstanding loan balance. This represents the principal amount yet to be repaid on the loan.

- Total Schedule Due Amount (P + I) - Calculates the premium fee on the total amount of the Principal and Interest due as per the upcoming repayment schedule.

- Total Schedule Due Amount (P + I + C) - Calculates the premium fee on the total amount that includes Principal, Interest, Instalment Fee and Loan Management Fee due as per the upcoming repayment schedule.

6. By default, the Restrict premium fee to max cover option is selected as No. If you select this option as Yes, then the insurance fee percentage basis calculation will be derived from the maximum cover of the insurance plan only when the current balance of the loan account exceeds the maximum cover of the insurance plan.

Example:

Insurance Cover = 100,000

| Current Balance in Loan | Restrict Premium Fee to Max Cover | Basis Amount to calculate Premium |

|---|---|---|

| 105,000 | Yes | 100,000 |

| 105,000 | No | 105,000 |

| 99,000 | Yes | 99,000 |

| 99,000 | No | 99,000 |

You can define Temporary suspension rules using the following:

7. Balance exceeding insurance cover option is selected as No by default. You can change it to Yes if you want the insurance plan to be suspended when the current balance in the account exceeds the Insurance Cover amount. If Temporary suspension is Yes and if Insurance fee basis is selected as outgoing balance, then the temporary suspension will get triggered when the outgoing balance is greater than insurance plan cover. The insurance will get reactivated when the current balance of the loan account goes below the amount of Insurance cover maintained.

8. Enter the minimum balance that is required for the insurance coverage in the Minimum balance for cover field. If the balance in the account is less than the Minimum balance to cover specified here, the insurance for the account will be temporarily suspended; and will be automatically reactivated when the balance in the account reaches the Minimum Balance to Cover.

9. If Balance Exceeding Insurance Cover is Yes or Minimum Balance for Cover is > 0, then the Suspension Basis will be Outgoing balance. Based on this Aura will check the outgoing balance (i.e., the Principal amount remaining unpaid on the loan) to suspend the insurance. The Suspension Basis is defaulted to Outgoing Balance and is not editable.

10. By default, Suspend on status will be selected as No and insurance plan will not be suspended when the loan moves to different Account Status or Payment Status. If Yes is selected, then Status pane with all the user defined statuses maintained at Admin > System codes > Generic definitions > Loan status definitions will be displayed. By selecting the loan statuses, you can define when the insurance plan needs to be suspended. When the loan account moves into any of the selected statuses, the insurance plan for the account will be suspended automatically; and will be automatically reactivated when the loan account status is moved to any Status that is not added to Suspend on Status pane.

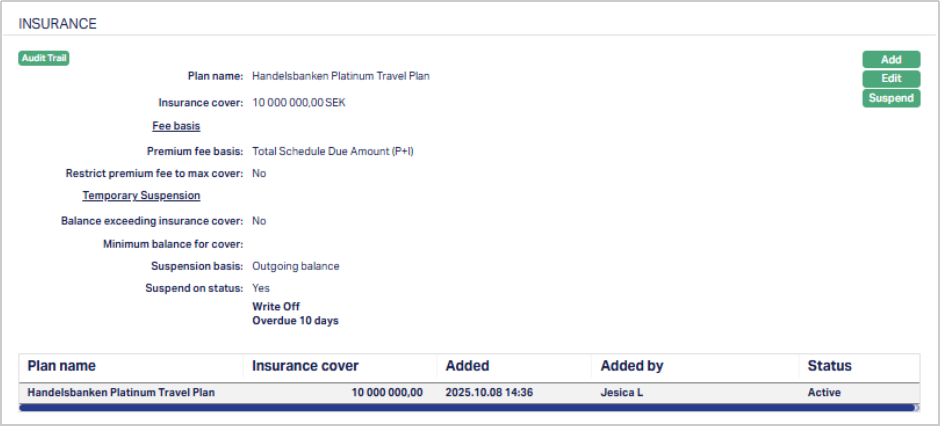

11. Click Save. The Insurance Plan tab appears with the added details.

Once saved, the Insurance Plan is linked to the Product and has an Active Status. Such Active Insurance Plans are available to all new loan accounts created under this Product, based on the parameters defined here.

Functions: Add, Edit, Suspend.

Note: When an insurance plan is mapped to a loan account under this Product, Aura automatically copies the following fields from the Product to the account level: Premium fee basis, Restrict premium fee to max cover, Balance exceeding insurance cover, Minimum balance for cover, Suspension basis, and Suspend on status. These fields are read-only at the account level. Aura uses the account-level values for all premium fee processing and automatic suspension logic.

If any of these fields are updated at the Product level after loan accounts have already been created, the changes do not apply to existing accounts. The account-level values remain as they were at the time the insurance plan was mapped. Only new accounts created after the update will reflect the revised Product configuration.

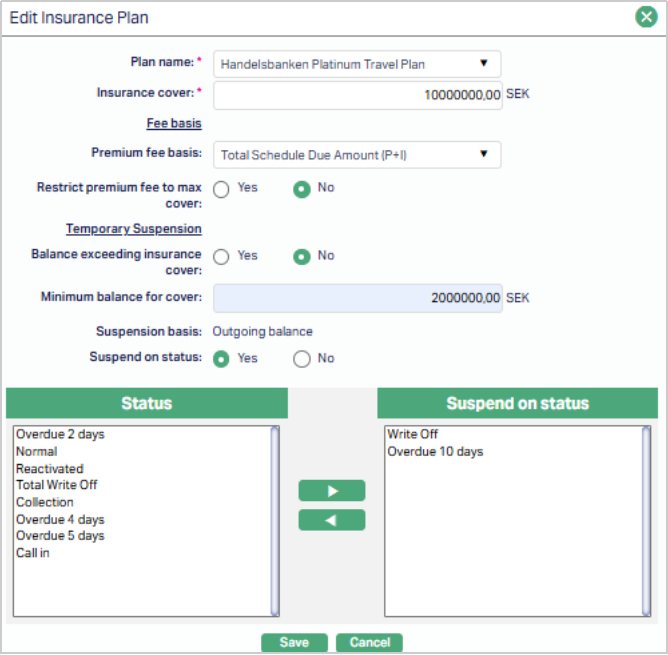

To edit the Insurance Plan,

1. Click Edit. The Edit Insurance Plan page appears.

Note: All fields under Edit Insurance Plan are editable.

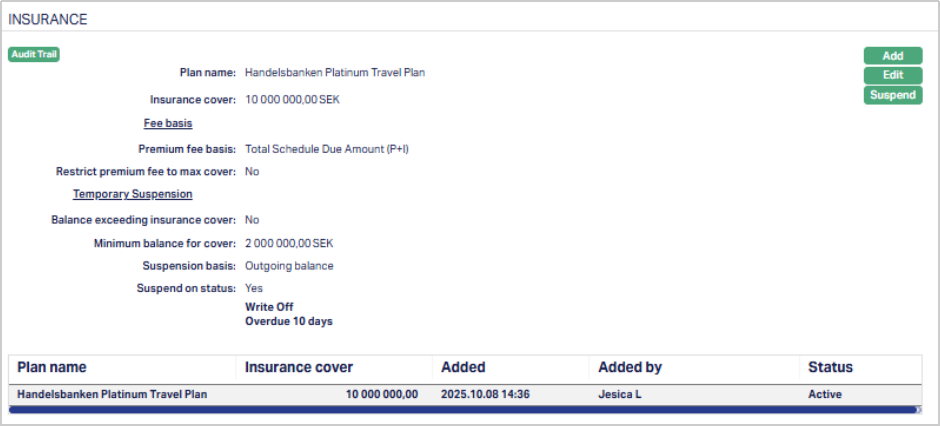

2. Click Save. The Insurance Page appears with the edited details.

Functions: Add, Edit, Suspend.

Suspend: You can suspend an Insurance Plan record by clicking on the Suspend button. When you click on the Suspend button, Aura will ask for confirmation. On confirmation Aura will suspend the Insurance Plan and the Activate button will appear in place of the Suspend button. The status of the Insurance Plan is set to Suspended. Such suspended Insurance Plans will no longer be available for loan accounts created under the Product after such suspension.

Activate: If you want to activate a suspended Insurance Plan record then click on the Activate button. Aura will ask for confirmation. On confirmation Aura will activate the Insurance Plan and the Suspend button will appear in place of the Activate button. The status of the Insurance Plan is set to Active. Only such Active Insurance Plans will be available for loans created under the Product.

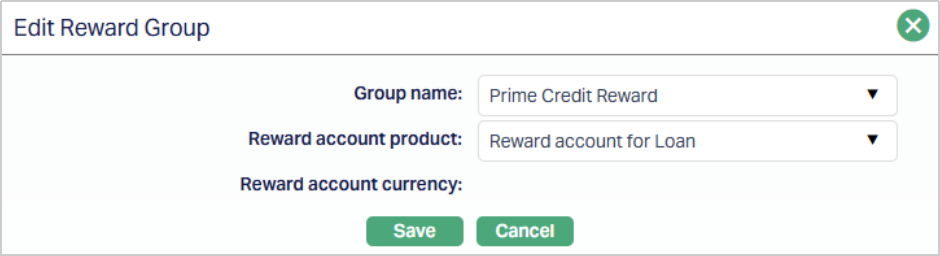

Reward Group

The Reward Group tab allows you to associate a Reward Group with the selected Loan Product. The Reward Group defines the generic rewards applicable to all loan accounts created under this Product. Any loan account created under this Product will automatically inherit the rewards mapped to the associated Reward Group.

To view / edit a Reward Group,

1. Access the Product Maintenance page. Click on Profile tab and select the Reward Group tab. If any Reward Group has already been added, these would be displayed; else, it will be blank.

2. Click Edit. The Edit Reward Group page appears.

3. Select the required Group from the drop-down list under Group name. The list displays all active Reward Groups defined under CRM → Loyalty Program → Settings → Reward Group that are available for Mortgage & Loan Products. Once you save the mapping, the selected Group Name becomes a hyperlink that redirects you to the corresponding Reward Group record for detailed viewing or maintenance.

4. Select the Reward account product from the drop-down list of active Reward Account Products maintained under CRM → Loyalty Program → Settings → Product. This Product will be used to create Reward Accounts for maintaining reward accrual and redemption transactions.

5. Reward account currency displays the reward currency associated with the selected Reward Account Product as defined under CRM → Loyalty Program → Settings → Product. This field becomes mandatory when you select the Reward Account Product.

6. Click Save. The Reward Group tab is displayed with the added details.

Function: Edit

Once you save the details, the selected Reward Group and Reward Account Product are mapped to the Loan Product. This mapping defines which reward configuration and reward account setup will apply to loans created under this product.

You can edit the Reward Group setup at any time. After the edit is approved, the updated configuration will apply only to loans disbursed after the change.

You can modify the Reward Group or the Reward Account Product as required. When a new Reward Account Product is selected, the Reward Account Currency field becomes conditionally mandatory and displays only the currencies linked to the selected Reward Account Product.

Note: The list of Reward Groups displays only Active Reward Groups where the Product Type = Mortgage and Loans. For details on how the selected Reward Group behaves at the Loan Account level - such as how rewards are generated, validated, or replaced, refer to the Loan Account → Reward Tab user manual.

Changes made in the Reward Group tab are subject to approval as per standard Product Maintenance workflow.

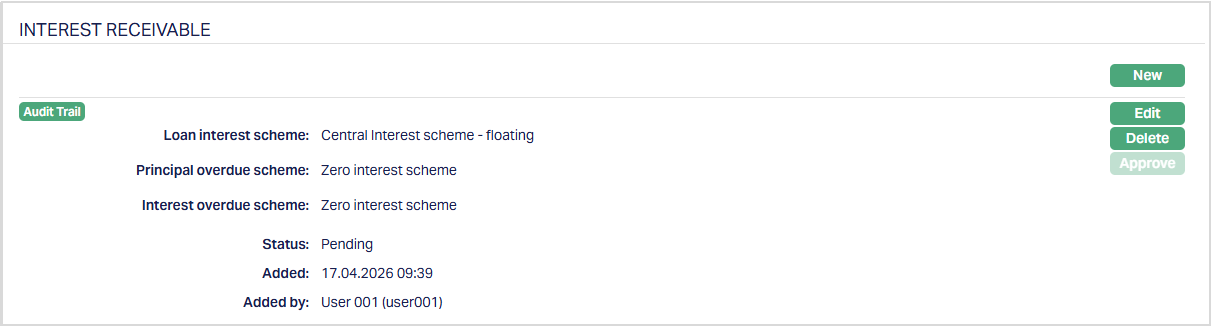

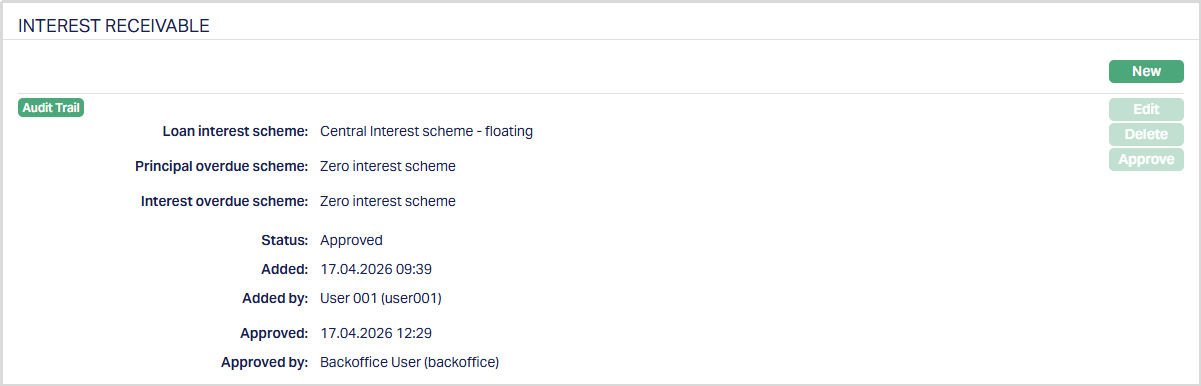

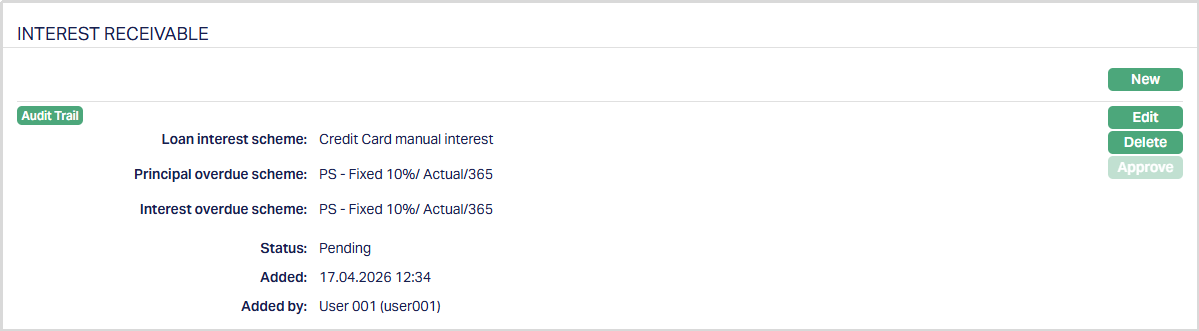

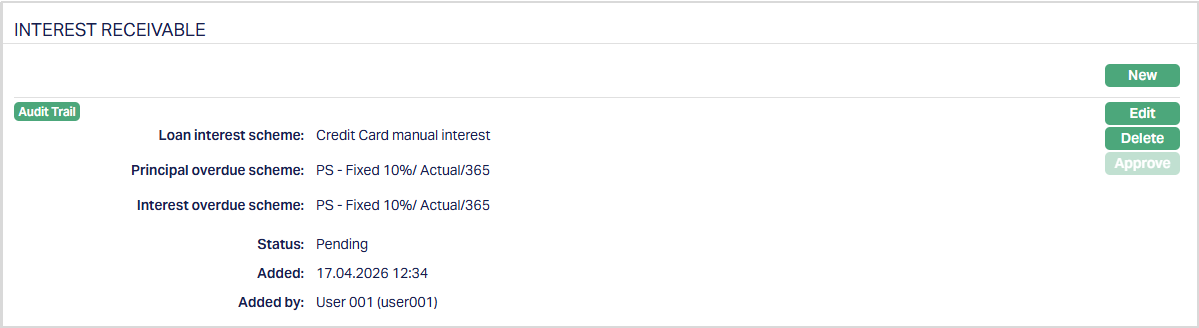

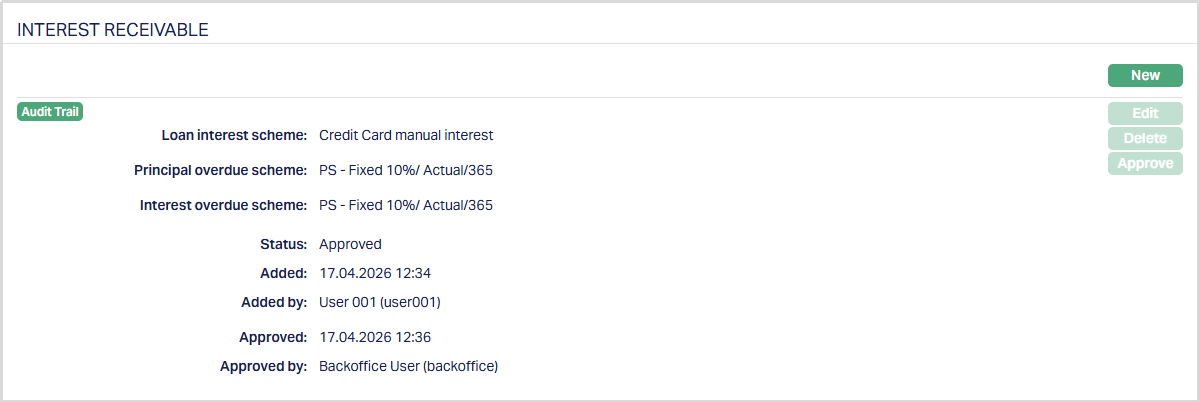

Interest Receivable

This tab allows you to create and maintain the various interest schemes for the interest chargeable on the loan accounts under this Product. You can define the interest schemes applicable for the interest on the Loan Principal as well as the Penalty interest on any overdue Principal / Interest.

To view / add Interest Receivable,

1. Access the Product Maintenance page. Click on the Interest Receivable tab to view the details as per sample below. The details are defaulted from the entries that you made during Product creation / last edit. For details refer to Mortgage and Loan → New Product → Interest Receivable (4/10).

Notes:

After creation / edit, the tab is in Pending status.

When the status is Pending, the interest receivable record can be edited only by the user who created the record; however, it can be deleted by any user by a click on Delete.

To approve, a user different from the one who created / edited has to retrieve the record and click Approve. Once the tab is approved and the red bubble disappears, no further changes can be done on the Interest Receivable tab.

If you want to change any settings for the Interest receivable tab for the Product after it is approved, you have to use the New button and create a new Interest Receivable record.

The additional fields that you can view in the Interest Receivable tab are explained below.

Status field denotes the status of the record.

Added field denotes the date on which the record was added.

Added by field denotes the name of the user who created the record.

Approved field denotes the date on which the record was approved and is displayed only on approval.

Approved by field denotes the name of the user who approved the record and is displayed only on approval.

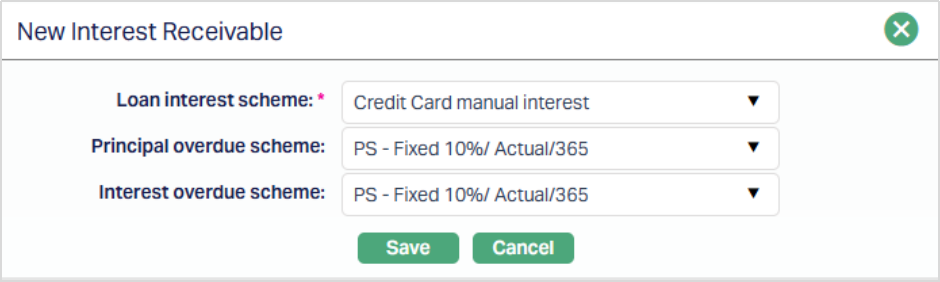

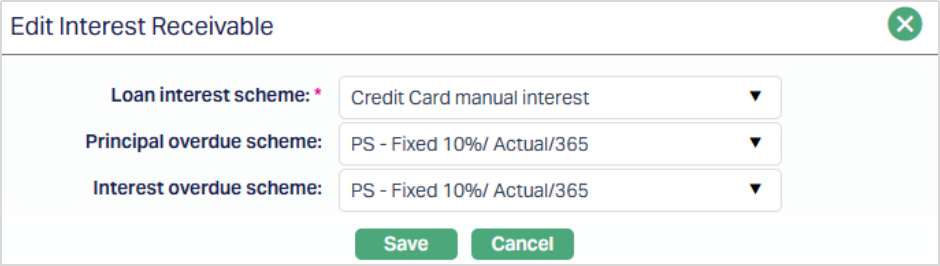

2. Click New. The New Interest Receivable page appears.

Enter the details as explained in the section New Product → Interest Receivable (4/10).

Enter the details as explained in the section New Product → Interest Receivable (4/10).

3. Click Save. The Interest Receivable page appears with the added details.

Functions: New, Edit, Delete and Approve.

To edit the Interest Receivable details,

1. Access the Product Maintenance page. Click on the Interest Receivable tab to view the details as per sample below. The details are defaulted from the entries that you made during Product creation. For details refer to Mortgage and Loan → New Product → Interest Receivable (4/10).

2. Click Edit. The Edit Interest Receivable page appears.

All the fields are editable during Edit Interest Receivable. However, only the person who created the interest receivable record can edit it, till it is approved.

3. Make the required changes and click Save. Once Saved the Interest Receivable page appears with the edited details as shown below.

Functions: Edit and Delete

Note: To approve, a user different from the one who created / edited has to retrieve the record and click Approve. Once the tab is approved and the red bubble disappears, no further changes can be done on the Interest Receivable tab.

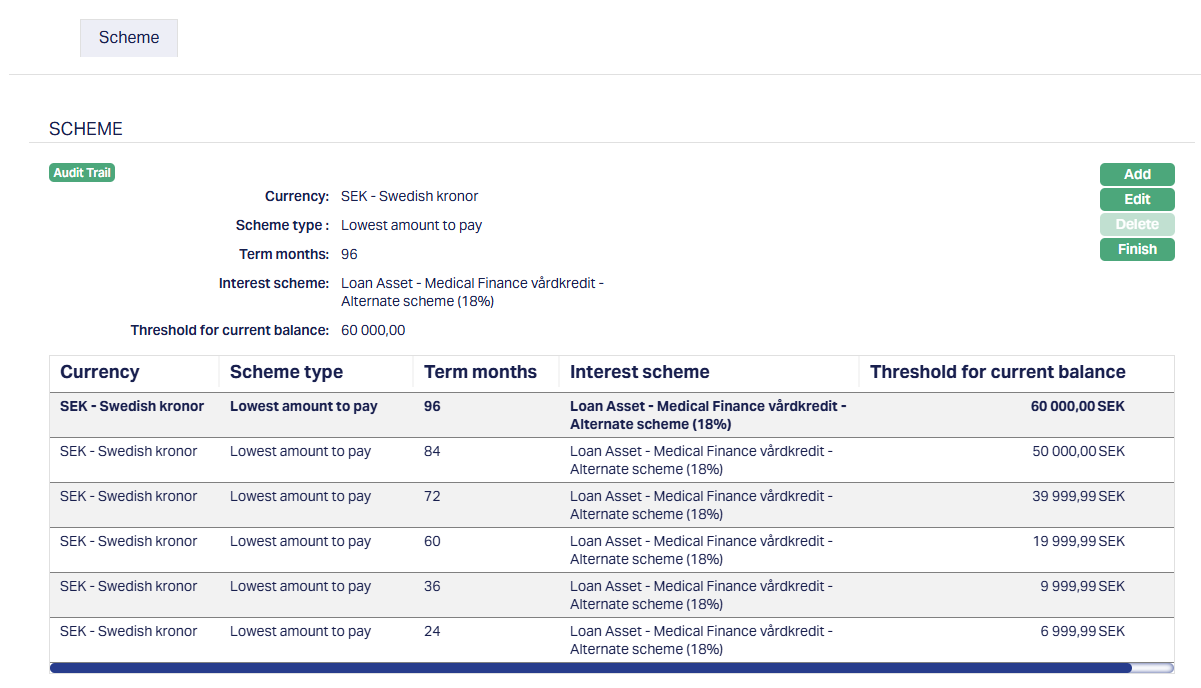

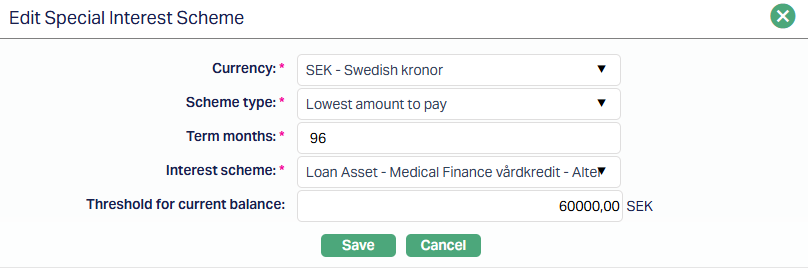

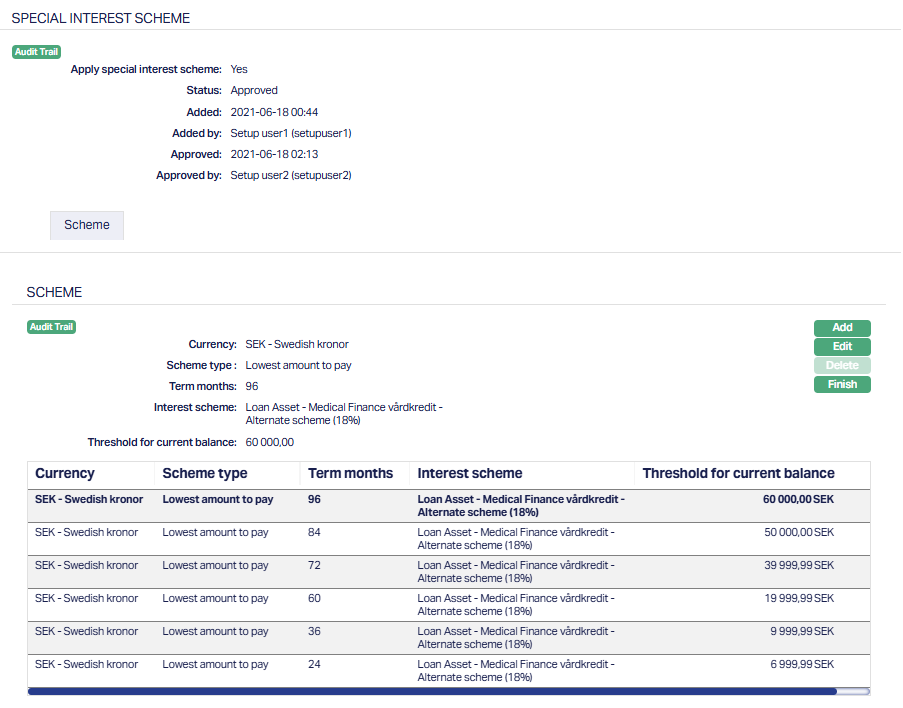

Special Interest Scheme